Between April 1 and April 8, 2026, three federal agencies put concrete proposals on the table for how the GENIUS Act will be implemented.

- Treasury issued its notice of proposed rulemaking (NPRM) on how state-level stablecoin regimes get certified as substantially similar to the federal framework.

- The FDIC published a NPRM establishing requirements and standards applicable to FDIC-supervised permitted payment stablecoin issuers (PPSIs) and insured depository institutions (IDIs) that engage in payment stablecoin-related activities, covering reserves, redemption, custody, and risk management.

- FinCEN and OFAC jointly proposed the AML/CFT and sanctions compliance program that every PPSI will need to build.

🗓️ April 1: Treasury defines the pathway to state-level regulation

The GENIUS Act created a dual-pathway regime. Payment stablecoin issuers with consolidated outstanding issuance of $10 billion or less can opt into state-level regulation, provided the state regime is certified as "substantially similar" to the federal framework. Issuers above that threshold come under direct federal oversight.

Treasury's April 1 NPRM lays out the broad-based principles it will use to determine substantial similarity, building on the advance notice of proposed rulemaking Treasury issued the prior September.

Under GENIUS, states must meet or exceed the core prudential standards and requirements described in Section 4(a) of the Act. Treasury's proposal splits those Section 4(a) requirements into two buckets:

- "Uniform requirements" (such as reserve composition, BSA/sanctions compliance, and redemption obligations), where states have essentially no interpretive discretion and must mirror the federal standard.

- "State-calibrated requirements" (such as capital, liquidity, reserve asset diversification, and risk-management standards), where states retain meaningful design flexibility but must still produce outcomes "at least as stringent and protective" as the federal framework.

For provisions outside Section 4(a) — applications, licensing, supervision, and enforcement — states get more latitude, but must still deliver similar levels of authority, oversight, and holder protection. Examination authority, for example, cannot be limited to cases where the issuer consents, and stablecoin holders cannot be treated as general unsecured creditors in insolvency.

Treasury is also explicit that states may go beyond federal requirements, but only if the additional rules neither conflict with the Act nor erode the substantially-similar determination.

The comment period runs 60 days from Federal Register publication.

🗓️ April 7: FDIC sets the operating rules for PPSIs

On April 7, 2026, the FDIC approved a NPRM implementing GENIUS Act requirements for FDIC-supervised PPSIs and insured depository institutions that engage in payment stablecoin-related activities, with comments due by June 9, 2026.

Among the most consequential provisions is proposed § 350.3(b)(4), which operationalizes Section 4(a)(11) of the GENIUS Act — the statutory prohibition on stablecoin yield. The rule would bar a PPSI from paying any holder of its payment stablecoin any form of interest or yield, whether in cash, tokens, or other consideration, solely in connection with the holding, use, or retention of the stablecoin.

Anticipating that issuers may seek to replicate yield indirectly through affiliates or commercial partners, the FDIC pairs the prohibition with a rebuttable presumption. An issuer is presumed to be in violation if it has an arrangement to pay consideration to an affiliate or related third party, and that affiliate or related third party in turn pays interest or yield to holders of the issuer's stablecoin solely for holding, using, or retaining it. The presumption also reaches cases in which the PPSI issues stablecoins on behalf of, or under the branding of, a related third party — in that scenario, the end holder is treated as a holder of the PPSI-issued stablecoin for purposes of the prohibition.

That second prong is aimed squarely at white-label and co-branded issuance arrangements, where the regulated issuer is one entity but the customer-facing brand and distribution relationship sit with another.

A PPSI may rebut the presumption only by submitting written materials that satisfy the FDIC the arrangement is neither prohibited nor structured to evade the prohibition. Taken together, the provision signals that the FDIC intends the no-yield rule to apply substantively, not just on the face of issuer–holder documentation.

🗓️ April 8: FinCEN and OFAC define the AML/CFT and sanctions rules

On April 8, 2026, FinCEN and OFAC jointly issued a proposed rule implementing the GENIUS Act's directive to treat PPSIs as financial institutions under the Bank Secrecy Act and to require an effective sanctions compliance program. The rule puts PPSIs squarely under the full BSA playbook — a risk-based AML/CFT program, SAR filing (at a $5,000 threshold), Customer Due Diligence and beneficial ownership collection for legal entity customers, CTRs, Recordkeeping and Travel Rule, information sharing, enhanced due diligence for correspondent and private banking relationships, and special measures — plus two PPSI-specific obligations mandated by the GENIUS Act:

(1) technical capabilities to block, freeze, and reject impermissible transactions, and

(2) the capability to comply with "lawful orders" to seize, freeze, burn, or prevent the transfer of payment stablecoins.

On the sanctions side, OFAC proposes a new Part 502 codifying a five-element effective sanctions compliance program (senior management commitment, risk assessment, internal controls, testing and auditing, and training), modeled on OFAC's 2019 Compliance Framework and 2021 Virtual Currency Industry Guidance.

On Travel Rule specifically: FinCEN's 2019 interpretive guidance (FIN-2019-G001) had already clarified that transmittal orders involving convertible virtual currencies (CVCs) — a category that includes payment stablecoins — qualify as "transmittals of funds" under the Recordkeeping and Travel Rules, because a CVC transmittal order is an instruction to pay "a determinable amount of money." The underlying Travel Rule obligation therefore already applied. What is new is that FinCEN proposes amending the definition of "transmittal order" in 31 CFR 1010.100(eee) to expressly include payment stablecoin alongside "money", codifying the 2019 position and removing any remaining room for interpretation post-GENIUS. PPSIs are also being added to the list of institutions in § 1010.410(e)(6), giving them the same PPSI-to-PPSI and PPSI-to-bank exceptions that banks and broker-dealers enjoy.

The relevance of Travel Rule requirements extends well beyond Travel Rule compliance in itself. OFAC sanctions are a strict-liability regime — a PPSI can be held civilly liable for a violation even without knowledge that it was engaging in one — and the rule makes clear that PPSIs must account for identifying and blocking transactions that would violate U.S. sanctions, including stablecoins traded by blocked persons on the secondary market when a PPSI exercises possession or control (for example, through smart contracts). A risk-based OFAC program cannot function on wallet addresses alone; meaningful screening requires counterparty identity. The data PPSIs collect through Travel Rule controls is paramount to ensure the effectiveness of OFAC screening programs.

Finally, proposed § 1033.240(a) implements the GENIUS Act's directive that PPSIs maintain technical capabilities, policies, and procedures to block, freeze, and reject specific or impermissible transactions, and FinCEN expressly extends this obligation to secondary market activity, noting that this is where the majority of illicit stablecoin flows occur.

Conclusion

Read together, these three proposals sketch the operational reality of PPSIs under the GENIUS Act. All three proposals follow the standard 60-day comment window from Federal Register publication, which puts the response deadlines in early June 2026. Overlaying this process is the GENIUS Act's own effective-date mechanic. The Act becomes effective on the earlier of (a) January 18, 2027, or (b) 120 days after the primary Federal payment stablecoin regulators issue final regulations implementing the Act.

Notabene is actively preparing its response to the FinCEN and OFAC NPRM. Further insights to follow.

Stablecoin payments shouldn't require your finance team to chase down wallet addresses, verify counterparties manually, or reconcile transactions after the fact. In this two-minute walkthrough, I demo how a custodial wallet provider can create and send a compliant invoice that gets paid, verified, settled on-chain, and reconciled — automatically — through Notabene Flow.

Last month, I joined government and industry stakeholders from both sides of the Atlantic at the U.S.–U.K. Transatlantic Taskforce on Markets of the Future. The session brought together U.S. Treasury, the FCA, the Bank of England, and agencies including the SEC, CFTC, FDIC, OCC, and Federal Reserve, alongside asset managers, global banks, payment platforms, and digital asset infrastructure providers.

The discussion was substantive and specific. Participants named real friction points: punitive Basel capital treatment keeping banks out of tokenized markets, definitional mismatches between U.S. and U.K. money market funds, sandbox structures that inadvertently exclude non-U.K. entities, and the gap between where stablecoin policy intent is heading and where operational realities sit today.

I want to share the perspective Notabene brought to the table as it cuts to something foundational that often gets lost in the broader regulatory harmonization conversation.

As tokenization and stablecoin settlement scale, the question is not whether we regulate — it's whether supervision is interoperable across jurisdictions.

Right now, the policy intent between the U.S. and U.K. is largely aligned. The operational realities are not. From Notabene's position — operating the largest AML Travel Rule-compliant network for regulated institutions, connecting thousands of counterparties across more than 100 jurisdictions and facilitating over $2 trillion in annual transaction volume — we see exactly where that friction lives. Here is where we focused.

Interoperability Is the Friction Point

The Travel Rule is not a niche crypto requirement. It is a core FATF standard designed to ensure that cross-border value transfers carry originator and beneficiary information. Over 100 jurisdictions are now implementing some version of it. Interoperability is no longer theoretical, it is foundational to how digital asset markets function safely across borders.

But the U.S. and U.K. implementations diverge in ways that create real, daily compliance asymmetry. In the U.K., firms must transmit core Travel Rule information for crypto transfers regardless of amount, with enhanced requirements once transfers exceed roughly €1,000 in cross-border contexts. In the U.S., Travel Rule obligations generally trigger at $3,000, with different implementation mechanics.

Even though the policies are aligned, that difference alone creates operational friction. A U.K. firm is obligated to receive information on a broader set of transfers than a U.S. counterparty is legally required to send. U.K. firms are also required to report non-compliant U.S. counterparties to the FCA — even where the U.S. counterparty transmitted no data because it had no obligation to do so under U.S. regulations.

This is not a disagreement about AML policy. Both jurisdictions are committed to the same underlying objective. It is a systems interoperability problem — and it has a tractable solution. Alignment on a minimum interoperable data schema and response protocol for cross-border regulated transfers would resolve it. The forthcoming adjustments to align with the revised FATF Recommendation 16 present a timely, concrete opportunity.

Trust Frameworks Should Be Machine-Readable

Both jurisdictions expect firms to conduct risk-based due diligence on counterparties — verifying regulatory status, Travel Rule compliance capability, and safeguards around transmitted personal data. That expectation is sound.

The execution is not. Today, that diligence is largely manual and duplicative. If a U.S. institution and a U.K. institution are both supervised entities, there should be a standardized, machine-readable way to recognize that status and its scope. Not a PDF exchange. A structured, interoperable counterparty trust taxonomy.

This reduces friction while strengthening assurance. That is harmonized supervision done well and critically, it does not require identical regulatory regimes. It requires a shared vocabulary for recognizing equivalent outcomes.

Programmable Compliance Solves the Irreversible Settlement Problem

One of the defining operational challenges in digital asset markets is that once a transfer settles, reversal is difficult. Returning funds can introduce operational, liquidity, and sanctions exposure which are the very risks compliance frameworks are designed to prevent.

U.K. guidance produced by the Joint Money Laundering Steering Group already contemplates confirmation mechanisms to ensure that beneficiary information aligns before value is finalized. That instinct is correct. Programmable compliance is where it becomes actionable.

A pre-settlement authorization layer, which was introduced as an infrastructure upgrade to virtual asset transactions, that allows institutions to validate identity, confirm regulatory status, attach structured compliance metadata, and enforce AML policy before assets move. That transforms the Travel Rule from a recordkeeping obligation into a preventative control.

As stablecoins increasingly serve as settlement rails for tokenized activity, pre-settlement authorization is not an enhancement — it is a prerequisite for safe cross-border scale.

Without interoperable pre-settlement controls, cross-border settlement risk does not stay constant as these markets grow. It scales with volume.

Regulator Visibility Requires Harmonized Protocols

Regulators on both sides of the Atlantic are flying partially blind when Travel Rule exceptions occur cross-border. Without shared reason codes or common escalation thresholds, a compliance failure that is visible to the FCA may produce no signal at all for a U.S. counterpart and vice versa.

Open messaging standards already exist that would enable structured, machine-readable compliance exchange. The Transaction Authorization Protocol (TAP) — the open standard that Notabene Transact and Notabene Flow are built on — is designed precisely for this: allowing verified entities to exchange compliance data securely and consistently before settlement. The point is not to mandate any single framework. It is to recognize that programmable interoperability is technically achievable today, and that aligning around open standards rather than bespoke bilateral integrations would materially reduce friction while strengthening supervisory oversight.

The Window Is Now

The session surfaced broader themes beyond Travel Rule mechanics — punitive Basel capital treatment keeping well-capitalized banks on the sidelines, definitional mismatches between U.S. and U.K. money market funds complicating tokenized collateral use cases, and open questions about how stablecoin issuance recognition will work across jurisdictions as the GENIUS Act moves into implementation.

Running through all of it was a consistent message from industry: we do not need identical rules. We need the rules we have to be interoperable. And we need that interoperability built into infrastructure — not achieved transaction-by-transaction through manual reconciliation.

What stood out about this session was the level of specificity on both sides. Regulators genuinely in listening mode. Industry participants naming concrete friction points rather than offering generalized calls for clarity. That is the right conversation to be having, and the right format for having it.

The taskforce indicated that recommendations will be delivered to the U.S.–U.K. Financial Regulatory Working Group this summer, ultimately reaching the Chancellor and Treasury Secretary. Written follow-up from industry is welcomed and encouraged.

For those who want to shape what comes next: now is the moment to be specific.

We’re excited to announce our integration partnership between Corsa and Notabene, bringing together leading transaction authorization and trust infrastructure with a modern risk operating system for moving digital assets compliantly and at scale.

Notabene provides real-time counterparty coordination and end-to-end transaction authorization solutions for digital asset businesses, enabling secure, compliant data exchange between counterparties. Institutions use Notabene to meet global regulatory requirements and facilitate high-value B2B stablecoin payments while maintaining seamless transaction flows. Corsa delivers the operating layer that unifies compliance data, automates workflows, and turns risk signals into actionable intelligence across the organization.

Together, the integration brings Notabene’s network-driven trust layer directly into the core of compliance operations and helps financial institutions bridge compliance decisioning and transaction execution.

With this integration, teams using Notabene can view Travel Rule information in full context - alongside counterparty data, transaction activity, customer profiles, onboarding data, alerts, and risk signals - all within Corsa.

By simply connecting their Notabene API keys, customers can automatically surface data from the Notabene network inside Corsa with no engineering work required. This securely encrypted data becomes immediately available across customer profiles, transactions, alerts, and investigations, enabling a unified and real-time view of compliance across both counterparties and transactions.

Beyond visibility, the integration enables companies to operationalize Travel Rule data within their broader compliance workflows. Teams can incorporate this data into monitoring, investigations, and decisioning processes - all within Corsa.This allows compliance teams to move beyond fragmented workflows and manage Travel Rule requirements as part of a broader, connected compliance system.

This partnership reflects a shared vision: enabling digital asset institutions to meet global regulatory requirements while moving value with greater speed, confidence, and control.

By combining Notabene’s trust infrastructure with Corsa’s unified compliance and risk OS, teams gain the ability to manage regulatory obligations and customer risk in one place - with full context, control, and automation.

---

For more info, talk to our team or visit www.corsa.finance

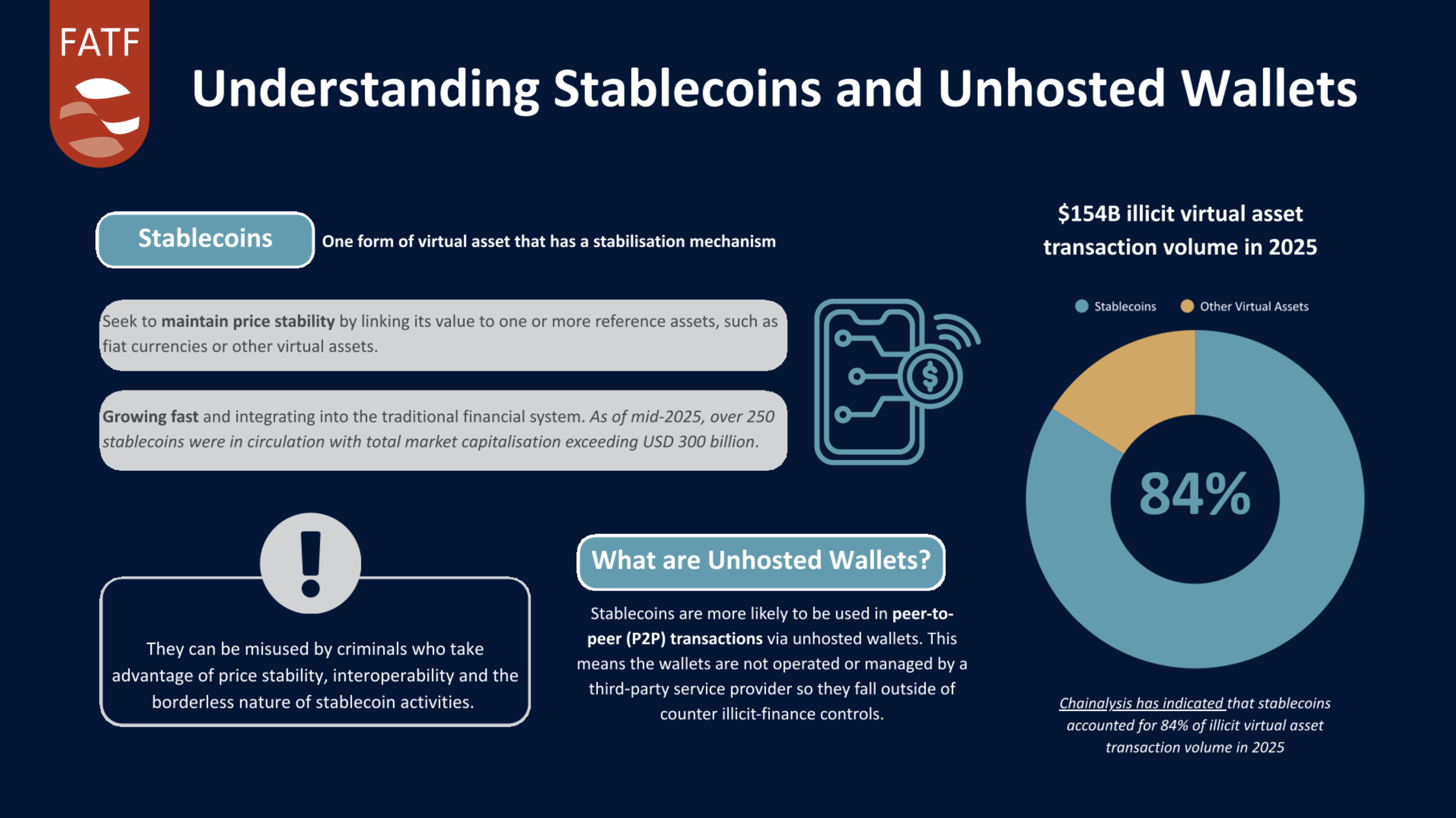

The Financial Action Task Force (FATF)'s March 2026 report on stablecoins and unhosted wallets is simultaneously alarming and clarifying. It formally documents the architecture of a compliance failure that we at Notabene have been watching for years.

The report finds that stablecoins now represent 84% of illicit virtual asset transaction volume, surpassing Bitcoin. As of March 2026, there are 259 stablecoins in circulation, with a combined market cap exceeding $300 billion. They're faster, more stable, and more liquid than Bitcoin—exactly the properties that make stablecoins useful for legitimate commerce. The problem is that these same properties make stablecoins attractive to DPRK state hackers, Iranian proliferation financiers, and professional money launderers.

FATF illustrates these dynamics in the infographic below, highlighting the growing role of stablecoins and the increasing use of peer-to-peer transactions through unhosted wallets.

The report notes that stablecoins are increasingly used in peer-to-peer transactions via unhosted wallets, which are not operated by third-party service providers and can fall outside traditional counter-illicit finance controls.

The real story here isn't the stablecoin adoption curve. it's the gap in the compliance framework built to contain it.

The Unhosted Wallet Problem

The FATF report doesn't frame stablecoins as the problem. Its focus is on how they move. Peer-to-peer (P2P) transactions via unhosted wallets are the critical vulnerability the report identifies, and within the current FATF framework, there's no regulatory solution to close it.

By design, P2P transactions between individuals using self-custody wallets fall outside AML/CFT obligations. This allows users to send and receive crypto assets without relying on a regulated intermediary like an exchange or custodian**.** No intermediary means no obliged entity responsible for customer due diligence, transaction monitoring, or suspicious activity reporting. The transaction is visible on-chain, but functionally invisible to competent authorities until it reaches an off-ramp.

This is a structural feature of the framework as written, not an implementation gap.

The FATF acknowledges this honestly. Their guidance as it pertains to Travel Rule coverage on this is clear: obligations fall on VASPs, not individuals. Secondary market P2P transactions don't trigger compliance requirements. However, the report documents case after case of threat actors exploiting this exact dynamic: layering in unhosted wallets, chain-hopping across blockchains, structuring transactions to stay functionally distant from any Travel Rule-covered wallet, then converting to fiat through unlicensed OTC brokers in jurisdictions with weak AML/CFT controls.

What the Report Gets Right

The FATF report makes clear that this is not a detection problem that can be solved with better analytics. The mitigation measures recommended such as identity verification of wallet owner, whitelisting (allow-listing), blacklisting (deny-listing), programmable smart contract controls, blockchain forensics, supervisory colleges, and public-private partnerships are all legitimate tools, and some jurisdictions are already putting them to use:

- Switzerland plans to implement on-chain allow-listing.

- France is deploying blockchain analytics.

- Japan has introduced explicit requirements on stablecoin issuers and intermediaries.

- Singapore has mandated enhanced due diligence for unhosted wallet transfers.

The progress is real, but the problem is that all of these measures are reactive. They freeze addresses after the fact, monitor secondary market circulation, catch exits - but they don't prevent the transaction from happening in the first place.

The Travel Rule Problem

The FATF report is careful but clear on a critical vulnerability: the Travel Rule framework struggles with unhosted wallet scenarios in precisely the way that matters for stablecoin misuse.

The report reiterates that Recommendation 15 and the Travel Rule remain the foundation of crypto AML compliance. Under FATF standards, jurisdictions must ensure that virtual asset service providers (VASPs) are licensed or registered, conduct customer due diligence, monitor transactions, and report suspicious activity, and that they transmit originator and beneficiary information for qualifying transfers. ****It's designed to ensure that compliance-aware intermediaries have visibility and can apply controls. The FATF guidance makes clear that even when a VASP customer is transferring to an unhosted wallet, the VASP must collect beneficiary information.

The problem is what happens next or more precisely, what doesn't.

When a VASP's customer transfers to an unhosted wallet, the VASP now has beneficiary information about an address it doesn't control. That address, in turn, may then transfer to another unhosted wallet. And another. And another. The report calls this the "transactionally distant" problem: threat actors create chains of unhosted wallets that are multiple hops away from any Travel Rule-covered wallet, deliberately fragmenting the transaction trail.

The VASP at the origin can report the first transfer, but once stablecoins land in an unhosted wallet, they're effectively outside the obligated entity network. A VASP monitoring its customer's outbound transfer to an unhosted wallet has limited visibility into what happens downstream. When stablecoins pass through five, ten, or twenty unhosted wallet hops before reaching an off-ramp, no single obliged entity has sight of the full transaction chain. Most importantly, no single obliged entity is responsible for filing a suspicious activity report on the layered transfers that occur outside the Travel Rule-covered ecosystem.

This is a major structural limitation of Travel Rule implementation. The Travel Rule was designed for transfers between obliged entities. It creates visibility at the edges—when stablecoins enter and exit the regulated perimeter—but it has no mechanism to create compliance visibility for movements within the unhosted wallet space.

The FATF acknowledges this by noting that stablecoin issuers may need to play a complementary role, using their ability to freeze or monitor addresses based on information from law enforcement. That ability is reactive, not preventive.

The Authorization Gap

This is where I keep returning to the question that animates much of our work at Notabene: what if the framework required authorization before the transaction, not just information exchange after?

The Travel Rule, as currently implemented, is fundamentally about information exchange and reporting the originator and beneficiary details flowing from one VASP to another, with suspicious activity reporting happening after transfers are processed. Unhosted wallet transactions bypass meaningful compliance precisely because once funds reach an unhosted wallet, they leave the obligated entity network entirely. Travel Rule visibility ends.

The framework needs to evolve beyond information exchange and toward pre-transaction authorization—specifically for flows involving unhosted wallets or chains of unhosted transfers.

The Transaction Authorization Protocol (TAP), an open standard protocol that embeds compliance directly into transaction settlement, is designed to solve exactly this problem. It complements the Travel Rule by adding an authorization layer that operates at the point of settlement, not just at the point of information exchange.

What Needs to Happen

The FATF report makes clear recommendations for jurisdictions: establish comprehensive legal frameworks, impose clear AML/CFT obligations on stablecoin issuers, assess and mitigate P2P risks, leverage advanced tools, and foster public-private collaboration.

But the report also, implicitly, shows the limits of the current approach. The existing framework allows for supervisory oversight of stablecoin issuers, enhanced due diligence for unhosted wallet transfers, mandatatory blockchain analytics, and address freezing.

None of these can prevent a compliant intermediary's customer from transferring stablecoins to an unhosted wallet controlled by a sanctioned entity, because the customer is acting on their own behalf, using tools available to them, and the transaction doesn't directly involve an obliged entity.

Notabene propose a two-fold response:

1. Push harder on implementing and strengthening the Travel Rule in the stablecoin ecosystem. The FATF requires VASPs to collect beneficiary information even for unhosted wallet transfers. But compliance with this requirement is uneven, and the tools for monitoring downstream transfers are limited. Jurisdictions need stronger enforcement of Travel Rule obligations, clearer standards for what beneficiary verification means for unhosted wallets, and better mechanisms for VASPs to share risk assessments when they know a customer is transferring to high-risk addresses.

2. The framework needs to evolve beyond the Travel Rule's information-exchange model, and toward pre-transaction authorization. The Transaction Authorization Protocol, also known as TAP — is a framework that embed compliance checks directly into transaction settlement—can close the visibility gap that the Travel Rule inevitably creates. Where the Travel Rule ensures that originator and beneficiary information is collected and reported, TAP would add a gate: real-time verification, risk assessment, and approval before settlement, with compliance rules embedded in the transaction itself.

The Travel Rule works when both parties are in the obligated entity ecosystem. TAP is designed specifically for the edge cases of transfers to unhosted wallets, cross-chain movements, and higher-risk scenarios where the Travel Rule's reach is limited.

For stablecoin issuers, this means embedding compliance logic into smart contracts that can enforce authorization requirements at the protocol level. A transfer to an unhosted wallet could trigger cryptographic ownership proof before settlement. Rules can be enforced not just through monitoring and remediation, but through the transaction mechanics itself.

This shifts responsibility from surveillance to prevention, and from ex-post reporting to ex-ante controls.

The DPRK's use of Tether to finance weapons procurement, Iranian actors converting stablecoins for components, terrorist financiers using densely structured wallet hops to move funds—these cases share a common thread. The privacy, liquidity, and pseudonymity built into the unhosted wallet architecture have become properties that existing compliance frameworks can't adequately address. The March 2026 FATF report documents this gap with precision.

The solution is not to abandon the Travel Rule, but to build solutions that extend its reach. Stronger enforcement of Travel Rule obligations on unhosted wallet transfers and open frameworks that bring compliance controls into the settlement layer itself are how we actually close this gap.

São Paulo/New York - 25 February 2026

Notabene, Veirano Advogados and ABToken announced today the launch of the Brazil Virtual Asset Regulatory Playbook, a practical implementation guide designed to help institutions navigate Brazil’s new regulatory framework for virtual asset service providers, including licensing, operational, AML/CFT obligations and Travel Rule requirements.

With the Central Bank of Brazil’s (BCB) new rules for virtual asset service providers (VASPs) now in force, Brazil enters a new phase of supervised virtual asset activity. The framework established by BCB Resolutions 519, 520, and 521 introduces a comprehensive licensing, supervisory, and AML/CFT regime for VASPs, as defined under Brazilian Law No. 14,478/2022.

Crucially, while Travel Rule obligations will be phased in through 2028, certain foreign exchange (FX) reporting requirements begin much sooner. Under BCB Normative Instruction No. 693, institutions must begin monthly reporting of FX-scoped virtual asset transactions, including self-hosted wallet and cross-border transfers, starting in May 2026. In practice, this means key originator and beneficiary data collection capabilities must be operational well ahead of full Travel Rule enforceability.

Designed for compliance, legal, operations, and product teams, the Brazil Playbook provides detailed guidance on:

- The VASP licensing framework and supervisory timelines;

- A breakdown of Travel Rule obligations under BCB Resolution 520;

- How foreign exchange reporting requirements intersect with Travel Rule controls; including the May 2026 monthly reporting obligation;

- The requirement for SPSAVs conducting FX-scoped activities to obtain both SPSAV and foreign exchange market licenses; and

- A phased implementation roadmap aligned to 2026 - 2028 enforcement milestones.

The Travel Rule framework under BCB Resolution No. 520 requires SPSAVs to collect, verify, retain, and transmit originator and beneficiary information for all virtual asset transfers, regardless of value. The guide outlines the two-phase rollout of Travel Rule obligations, beginning with domestic transfers between Brazilian VASPs and extending to cross-border transfers by 2028.

“Brazil’s new framework brings clarity, structure, and accountability to the virtual asset market,” said Catarina Veloso, Director of Regulatory & Compliance at Notabene. “The May FX reporting milestone makes it clear that institutions cannot wait until 2027 or 2028 to operationalize Travel Rule capabilities. This Playbook is built to help firms make meaningful progress throughout the two-year phased implementation period, while ensuring they meet interim regulatory milestones along the way.”

“The Central Bank’s regulations represent a structural shift in how virtual asset services are supervised in Brazil”, said Marcos Rocha, Partner at Veirano Advogados. “By clarifying the interaction between licensing, AML/CFT controls, and foreign exchange obligations, we aim to give market participants quick practical guidance.”

“This is a defining moment for Brazil’s virtual asset ecosystem,” said Regina Pedroso, Executive Director at ABToken. “Clear rules and coordinated implementation strengthen trust across the market and position Brazil as a leading jurisdiction for responsible innovation in virtual asset services.”

The Brazil Virtual Asset Regulatory Playbook is available for download now. Download the guide: https://notabene.id/reports/brazil-virtual-asset-regulatory-playbook

ENDS

About the Contributors

Notabene is the trust layer for global crypto money movement. Our products include Notabene Flow, the first open stablecoin payments platform for businesses, and Notabene Transact, the world's largest Travel Rule-compliant transaction authorization platform for regulated institutions. The Notabene network connects thousands of trusted counterparties, facilitating over $2T in transaction volume annually across more than 100 jurisdictions. It’s built on the Transaction Authorization Protocol (TAP), our open messaging standard that enables verified entities to transact securely. Notabene provides industry-leading tools for stablecoin payment coordination, real-time transaction authorization, counterparty verification, and self-hosted wallet identification—helping institutions build trust into every transaction.

Veirano Advogados is a leading Brazilian law firm with extensive experience advising clients in the fintech and digital assets industries. The firm has been closely involved in some of the most relevant projects in the Brazilian financial and crypto-asset markets, assisting both domestic and international clients on licensing, regulatory structuring, product launches, and complex cross-border transactions. Veirano’s team combines deep knowledge of the Brazilian financial regulatory framework with practical experience in the implementation of compliance programs, providing clients with pragmatic and business-oriented legal solutions in a rapidly evolving regulatory environment.

ABToken is a leading Brazilian industry association created to strengthen the country’s digital asset and tokenization ecosystem. The Association works to promote innovation alongside high standards of governance, regulatory compliance, and market integrity. ABToken represents tokenization platforms, blockchain companies, and virtual asset service providers (VASPs), serving as a unified voice for the sector in its engagement with regulators, policymakers, and market participants, and contributing to the development of a safe, credible, and sustainable digital finance environment in Brazil.

London / New York — 9 February 2026

Notabene today announces new regulated banking customer, AMINA Bank AG (“AMINA Bank”), a Swiss Financial Market Supervisory Authority (FINMA)-regulated crypto bank with global reach, to advance trusted infrastructure for transactions across crypto and traditional financial rails.

As digital assets continue to intersect with regulated finance, institutions on both sides are increasingly subject to the same regulatory expectations, even when operating on fundamentally different infrastructures. Standards developed for traditional finance, including FATF’s payment transparency requirements under Recommendation 16, have long been embedded in banking workflows. These expectations have since been extended to virtual assets and VASPs through the Crypto Travel Rule, creating a shared regulatory baseline across the two systems.

However, regulatory alignment has not translated into operational consistency. Differences in infrastructure, workflows, and counterparties mean that applying long-established expectations of counterparty trust to crypto transactions, particularly when value moves between the two environments, remains an operational challenge.

With this partnership, Notabene and AMINA Bank are addressing the real-world application of Travel Rule requirements across crypto-native infrastructure and regulated banking environments. Notabene’s platform enables secure information exchange and transaction transparency across crypto transactions. AMINA Bank provides banking services across traditional financial and digital assets in one place, serving clients from over 40 countries. Through this integration, AMINA Bank can now extend a more streamlined and automated experience for Travel Rule compliance.

“As institutional portfolios increasingly include crypto alongside traditional holdings, clients require infrastructure that works across both environments without creatng compliance friction,” said Myles Harrison, Chief Product Officer at AMINA Bank. “Integrating Notabene’s technology allows us to provide a more streamlined compliance framework that reduces operational friction, allowing clients to transact between crypto and traditional finance with ease.”

“FATF standards are well established in banking, but applying them consistently when value moves between crypto and traditional financial systems is still an open operational challenge,” said Pelle Braendgaard, CEO of Notabene. “AMINA is able to leverage the Notabene platform as a system of record for seamless, trusted transactions as these markets continue to converge.”

As the trust layer for global money movement, Notabene works with crypto-native firms and financial institutions to support secure information exchange, authorisation, and transparency across all transactions. Through partnerships such as the one with AMINA Bank, Notabene is moving the industry towards more consistent, operationally viable transaction flows between crypto and traditional finance.

This partnership marks an important step toward bridging operational and regulatory understanding between crypto and traditional finance, as institutions seek practical ways to support compliant, trusted digital asset activity within existing financial frameworks.

ENDS

Media Inquiries

We previously reported on Hong Kong’s new stablecoin issuer regime, which introduced a comprehensive set of Travel Rule obligations for licensed issuers. As the HKMA now moves from reviewing applications to making licensing decisions, issuers that treat Travel Rule as an afterthought risk delaying their go-live—operational readiness on Day 1 will be the real differentiator.

The Stablecoins Ordinance took effect on August 1, 2025, alongside the HKMA’s AML/CFT Guideline for licensed stablecoin issuers. The HKMA made clear that AML/CFT requirements—including Travel Rule compliance—apply to licensed stablecoin issuers.

The Guideline states explicitly in section 1.6 that the minimum AML/CFT criteria

“apply when a licensee is granted a license and continue to apply throughout the licensee’s conduct of licensed stablecoin activities.” HKMA AML/CFT Guideline for Licensed Stablecoin Issuers

In practice, the HKMA expects Travel Rule compliance to be addressed in the AML/CFT policies and procedures submitted as part of the license application. Once a license is granted, stablecoin issuers cannot commence operations until they are able to comply with the Travel Rule—meaning the necessary systems must be fully implemented, tested, and ready to go live before any regulated stablecoin activity begins.

The Ordinance included a transitional regime for entities already conducting regulated stablecoin activities before August 1, 2025, allowing eligible firms to continue operating while their license applications were assessed. This transitional window closes at the end of January 2026, with the HKMA able to grant provisional licenses up to February 1, 2026.

In practice, however, no entity actually benefited from the transitional regime, meaning there are no issuers operating under transitional status while awaiting approval.

The market is now entering the next phase: the HKMA is reviewing the first wave of applications, specifically those submitted by the end of September 2025, and expects to issue licensing decisions early this year.

The market is now entering the next phase: the HKMA is reviewing the first wave of applications, specifically those submitted by the end of September 2025, and expects to issue licensing decisions early this year. For applicants in this first cohort, the priority is to avoid a post-approval scramble—because the fastest route to launch is the one where operational compliance is ready before the license arrives.

For teams navigating this next phase of approvals and compliance readiness, join our upcoming webinar: HKMA Stablecoin Licensing Decisions Are Coming — Are You Ready?

What issuers should be doing now to protect go-live timelines

- Finalize your Travel Rule solution selection process and complete vendor due diligence

- Map end-to-end stablecoin transfer flows, including self-hosted wallet scenarios

- Approve detailed operating procedures and internal controls for stablecoin transfers

- Assess counterparty readiness, including messaging standards and data availability

- Integrate Travel Rule data into transaction monitoring and sanctions screening

- Produce evidence of testing and operational readiness, so compliance is demonstrable on Day 1

A closer look into Travel Rule obligations for Stablecoin Issuers

Scope of Application

The Guideline on Anti-Money Laundering and Counter-Financing of Terrorism (For Licensed Stablecoin Issuers) applies to stablecoin issuers that hold a license granted under section 15 of the Stablecoins Ordinance.

In the HKMA’s words:

“This Guideline is issued … for a stablecoin issuer which holds a license granted under section 15 of the Stablecoins Ordinance (hereafter referred as ‘licensee’). A licensee is a financial institution as defined in Part 2 of Schedule 1 to the AMLO.”

The HKMA is explicit that compliance with the Guideline is necessary to meet statutory obligations under both the Stablecoins Ordinance and the Anti-Money Laundering and Counter-Terrorist Financing Ordinance (AMLO).

“A licensee should meet these requirements in order to comply with the statutory requirements under the Stablecoins Ordinance and the AMLO.” HKMA AML/CFT Guideline

What that means in practice

- Only licensed stablecoin issuers are directly subject to these guidelines.

- Once licensed, the issuer is treated as an AML/CFT-obliged financial institution under Hong Kong law.

- The obligations apply to:

- the entity itself,

- its officers, senior management, and staff, and

- its licensed stablecoin activities, including issuance, redemption, and stablecoin transfers.

When the obligations apply

Importantly, the guidelines are not just ongoing supervisory expectations. They apply:

“when a licensee is granted a license and continue to apply throughout the licensee’s conduct of licensed stablecoin activities.”

This is why the HKMA expects applicants to demonstrate compliance readiness at the point of licensing, not after.

Who they do not directly apply to

- Unlicensed stablecoin issuers (though they cannot legally operate once licensing is required)

- Wallet providers, VASPs, banks, or intermediaries unless they are also licensed stablecoin issuers

- Overseas group entities, except to the extent group-wide AML/CFT controls are required by the licensed issuer (Chapter 3)

That said, counterparties do feel the impact indirectly, because licensed issuers must assess whether counterparties can meet Travel Rule and data-protection requirements before transacting with them (Chapter 6).

For pre-existing issuers operating under transitional arrangements, January marks the end of the window to continue business without a full license. For new applicants, January is when the HKMA starts deciding who's actually ready versus who's just talking about readiness.

Zero Tolerance for Compliance Gaps

Unlike jurisdictions that set minimum thresholds for Travel Rule compliance, Hong Kong takes a zero-threshold approach. Every stablecoin transfer requires travel rule compliance, regardless of amount. For transfers below $8,000, issuers must still collect and transmit originator and recipient names plus account information. Above $8,000, they need to transmit a broader scope of originator identifying information, as further detailed in our Hong Kong jurisdiction page.

End-to-end Travel Rule processes

Chapter 6 of the Guideline sets out detailed obligations for ordering, intermediary, and beneficiary institutions, in which they need documented procedures for collecting and verifying originator and beneficiary information, transmitting required data immediately and securely, and rejecting or escalating transfers with missing information. For more details, consult our Hong Kong jurisdiction page.

A functioning Travel Rule technology solution

If you rely on a third-party Travel Rule solution, the responsibility still sits with you. The HKMA requires due diligence proving your solution can identify counterparties, transmit data securely in real-time, handle transaction volume, and support sanctions screening.

Counterparty due diligence

Travel Rule compliance depends on who you transact with. The HKMA requires issuers to assess whether counterparties can meet Travel Rule and data-protection obligations before entering into stablecoin transfer relationships.

This is particularly important given the global patchwork of Travel Rule implementation. Issuers must be able to justify why a counterparty is acceptable or restricted.

Integration with monitoring and sanctions screening

Travel Rule data isn’t standalone. The HKMA expects it to feed into transaction monitoring and sanctions screening programs under Chapters 5 and 7 of the Guideline.

That includes screening originators and beneficiaries before executing transfers and using Travel Rule information to detect suspicious activity.

Self-hosted Wallets Get Enhanced Scrutiny

The guidelines take a particularly cautious approach to self-hosted wallet transactions. Stablecoin issuers must:

- Screen wallet addresses against databases of illicit activity

- Implement enhanced monitoring for higher-risk wallets

- Apply transaction limits where appropriate

- Collect originator/recipient information for all transfers to/from unhosted wallets

For more details, consult our Hong Kong jurisdiction page.

Ongoing monitoring

The HKMA recognizes that stablecoin transactions are visible on-chain and that tools like blockchain analytics, wallet screening, blacklists, and freezing mechanisms can help detect and respond to illicit activity. However, the HKMA takes the view that “the effectiveness of these risk mitigating measures is yet to be proven”—especially for peer-to-peer transfers involving self-hosted wallets—the HKMA expects issuers to take a cautious approach. This means that unless an issuer can clearly demonstrate that its risk controls are effective, the HKMA’s default expectation is that the identity of every stablecoin holder should be verified, even where that holder is not a customer of the issuer. In practice, this can create an obligation to verify the identity of third parties, either directly by the issuer or via a supervised financial institution/VASP or another reliable third party.

Operational readiness is your competitive edge

With the HKMA reviewing the first applications, Hong Kong’s stablecoin regime is moving from paper to practice. The framework sets a high bar, and issuers that can translate policies into operational capability will be better positioned to launch quickly once licensed. Travel Rule compliance, in particular, needs to be designed into the operating model from the start—it can’t be treated as a bolt-on—because it shapes everything from customer flows to monitoring, investigations, and SAR reporting. As licensing decisions begin to come through, the first-to-market issuers will be those that can demonstrate readiness and begin operating without delay.

For teams navigating this next phase of approvals and compliance readiness, join our upcoming webinar: HKMA Stablecoin Licensing Decisions Are Coming — Are You Ready?

The Digital Asset Market Clarity Act is the most comprehensive effort so far to establish a federal framework for digital assets in the United States. While much of the debate has focused on securities classification and innovation, the bill’s most consequential shift sits elsewhere, specifically in how it governs illicit finance and the movement of funds.

Rather than treating compliance as an afterthought applied after transactions occur, the proposed bill advances a different premise: that payment integrity must be built into the transaction itself. This approach aligns digital asset markets with long-standing expectations in traditional finance, where authorization, counterparty assurance, and traceability are prerequisites—not afterthoughts—for moving money.

Anti-money laundering controls, sanctions compliance, and the Travel Rule are no longer framed as constraints on innovation. They are framed as the trust infrastructure required for digital assets to function as real payment rails.

This is not about reinventing financial crime compliance. It is about extending it deliberately into digital asset markets, and in doing so, laying the foundation for crypto payments that institutions, regulators, and users can trust.

Bringing digital asset intermediaries under the Bank Secrecy Act

Title II explicitly places digital commodity brokers, dealers, and exchanges under the Bank Secrecy Act (BSA).

Section 201 removes any remaining ambiguity about whether crypto intermediaries are covered financial institutions. It directs the Treasury, through FinCEN, to apply AML and counter-terrorist financing requirements in a risk-based manner, consistent with how banks and payment providers are supervised today.

That includes:

- Risk-based AML/CFT programs

- Customer identification and due diligence

- Recordkeeping and suspicious activity reporting

- Compliance with U.S. sanctions administered by OFAC

This matters because BSA coverage is the legal foundation for the Travel Rule. Once an entity is clearly in scope, requirements to collect, transmit, and retain originator and beneficiary information are no longer theoretical, they are enforceable.

The Travel Rule: reinforced, not reinvented

The bill does not rewrite the Travel Rule. Instead, it strengthens the legal perimeter that allows it to function in digital asset markets.

Two provisions are critical:

First, by confirming that digital commodity intermediaries are BSA-covered institutions, the bill eliminates arguments that crypto transfers fall outside the transmittal-of-funds framework altogether.

Second, Title III, Section 303 introduces a special measure for certain transmittals of funds, modeled on Section 5318A of the BSA. This is the same authority Treasury uses to restrict or cut off transactions involving jurisdictions, institutions, or transaction types that present elevated money laundering risk.

Applied to digital assets, this authority allows Treasury to condition, monitor, or prohibit specific crypto fund flows where transparency or compliance breaks down.

The bill reinforces this approach further by explicitly including digital assets in the definition of monetary instruments, closing any remaining gap between crypto transfers and established concepts of value transmission.

Why the Travel Rule makes crypto payments safer

The Travel Rule is often framed as a compliance burden. In practice, it’s a basic safety mechanism.

By requiring originator and beneficiary information to accompany a transaction, the Travel Rule creates accountability across payment chains. It allows institutions to assess counterparty risk before execution, rather than relying solely on post-transaction monitoring.

This is how traditional payment systems work. Wire transfers, correspondent banking, and cross-border settlement depend on shared information standards to function safely.

Without those standards, payments become fragmented and high-risk. The same is true in crypto. When no one knows who is sending or receiving value, legitimate actors pay the price and illicit actors benefit.

The Travel Rule is about authorization and risk management. It enables compliant institutions to transact with confidence and limits the ability of bad actors to exploit opacity.

From transaction monitoring to transaction authorization

Another important shift in the bill is its emphasis on pre-transaction controls, not just after-the-fact reporting.

Several provisions authorize temporary holds, enhanced scrutiny, or conditions on execution where illicit finance risk is elevated. This brings crypto compliance closer to how mature payment systems actually operate.

In traditional finance:

- Certain payments require additional review before execution

- High-risk transfers may be delayed or blocked

- Authorization workflows are built directly into payment rails

By explicitly addressing digital asset transmittals within the BSA framework, the bill opens the door for similar controls in crypto especially for institutional, cross-border, and high-value transactions.

This reflects a simple reality: reporting suspicious activity after value has moved is often too late. Preventing abuse requires the ability to stop or condition transactions before settlement.

Payments transparency as operational infrastructure

Title II treats payments transparency as an operational requirement, not a policy aspiration.

The bill:

- Encourages the use of blockchain analytics in AML programs

- Expands examination standards for digital asset firms

- Directs attention to mixers, kiosks, and offshore intermediaries

It also focuses enforcement at key access points, such as digital asset kiosks and user-facing application layers. Even where underlying protocols are decentralized, the interfaces that enable access are expected to screen for sanctions exposure and high-risk activity.

This reflects how illicit finance actually works. Risk concentrates at entry and exit points, not deep inside protocol code.

Transparency at these points allows regulators to distinguish lawful activity from abuse—and allows compliant institutions to transact without assuming unnecessary risk.

What this means for crypto payments

Taken together, the illicit finance provisions of the Digital Asset Market Clarity Act point to three clear conclusions:

- Crypto payments will be held to the same standards as traditional payments

- Including AML controls, sanctions screening, and Travel Rule compliance.

- Risk assessment is moving closer to execution

- Authorization, not just monitoring, becomes central to compliance.

- Compliance is a condition for access, not a barrier to innovation

- Firms that cannot support transparency and authorization will struggle to connect to regulated payment networks.

The bill doesn’t solve every implementation challenge. But it draws a clear line: crypto payments that connect to the U.S. financial system must be traceable, authorizable, and accountable.

That’s how crypto payments become infrastructure—not an exception.

So what’s next: from markup to the President’s desk

The Clarity Act has already cleared an important milestone: it passed the U.S. House of Representatives with bipartisan support. The bill now moves to the Senate.

The next major milestone is markup, where the Senate will decide whether to take up the House-passed bill as written or advance its own version. That process includes committee review and potential amendments, particularly around market structure and illicit finance provisions. If the Senate’s version differs, the two chambers will need to reconcile the text before final passage.

Only once both the House and Senate pass identical language can the bill be sent to the President for signature.

Even then, the work won’t be finished. Much of the real impact will come through Treasury and FinCEN rulemaking, which will determine how AML, sanctions apply in practice especially for transaction authorization and cross-border crypto payments.

For compliance and payments teams, this is a key moment. The direction is set: crypto payments connected to the U.S. financial system will be expected to meet the same trust standards as traditional payments. What’s still being decided is how those standards are implemented.

Have questions about how this legislation might impact your business? Schedule a call with our Regulatory & Compliance team—we’d be happy to provide our perspective help you navigate this new regulatory landscape.

In 2025, the conversation around crypto and stablecoins fundamentally changed.

What was once framed as innovation at the bleeding edge of technology became infrastructure at the center of how financial organizations do business. Regulations matured, transaction volumes surged, and institutions moved decisively from experimentation to execution. In this environment, trust was no longer an aspiration. It became a prerequisite for scale.

For Notabene, 2025 was the year our founding vision became undeniable to the rest of the crypto and financial worlds. When the Financial Action Task Force (FATF) extended the Travel Rule to crypto in 2019, much of the industry viewed it as added friction—a compliance requirement imposed on a fast-moving ecosystem. At Notabene, we saw something fundamentally different.

We saw a catalyst for building what crypto had been missing since day one: a transaction authorization layer that enables digital assets to function as essential financial infrastructure. That belief has guided our work from the start, and in 2025 it began to fully take shape on Notabene as a powerful platform for trusted, programmable and revenue-generating transactions across the globe.

As the market evolved, so did our platform.

In 2025, Notabene evolved into a core payments infrastructure provider and system of record for financial institutions globally

.png)

That evolution was anchored by the launch of Notabene Transact, our next-generation transaction authorization and compliance engine.

Transact is the operational core of the Notabene platform and the system of record that regulated financial institutions rely on to move digital assets at scale. It is where counterparty due diligence, policy enforcement, and transaction authorization come together in real time, enabling institutions to make automated, risk-aware decisions before value moves.

By embedding compliance and authorization directly into transaction flows, Transact enables high straight-through processing rates while meeting the regulatory requirements of operating across jurisdictions. What began as Travel Rule infrastructure has evolved into a foundational layer that institutions depend on to operate, scale, and connect with confidence on the Notabene Network.

When we started Notabene, we saw compliance as a critical stepping stone—the core—but not the end goal. Enabling compliant transactions at scale meant starting with the hardest problem first: getting compliance right. The vision was to embed trust directly into how transactions are authorized, coordinated, and settled so that digital assets could support real-world payments at scale. We made this possible last year with the launch of Notabene Flow, the first open stablecoin payments platform built for businesses.

Notabene Flow introduces new payment capabilities such as pull payments and recurring subscriptions, enabling our fast-growing network to provide instantaneous stablecoin payments to the global B2B market. It also represents a shift from enabling individual transactions to enabling complete payment workflows that meet both operational and regulatory expectations.

By embedding compliance, identity, and authorization directly into payment flows, Notabene Flow takes stablecoins beyond simple transfers and into real commercial use, enabling new revenue flows for institutions in our network. It is a critical step toward making stablecoins usable at scale in everyday business.

When we look back at 2025, a few themes become clear to us.

Growing transaction volume across borders requires a built-in trust layer

In crypto’s early years, compliance was often treated as an add-on, implemented only when regulation made it unavoidable—and as a result, it was frequently viewed by business teams as friction rather than an enabler. By 2025, that mindset no longer held.

As transaction volumes grew and stablecoins moved into real payment flows, trust could no longer be bolted on after the fact. Growth itself began to require shared standards, interoperability, and regulatory alignment built directly into how value moves.

That shift was not anecdotal. It was visible in the data and in the scale of the Notabene Network, which by Mid-2025, surpassed $1 trillion in total transaction volume processed across our network. While the first $500 billion took us three and a half years to grow into, the second happened in just 6 months. This exponential growth trend continues with the Notabene Network knocking on the door of $2T just a few months later.

This milestone reflects both the scale at which our customers operate and the role Notabene plays in enabling compliant global transactions. As institutions handle higher volumes across more jurisdictions, Notabene increasingly serves as the connective infrastructure that allows crypto and stablecoin payments to move safely between counterparties.

Compliance became an enabler of doing business for anyone working with digital assets

As regulatory expectations moved from concept to enforcement across 2025, one question dominated the industry: Is the market ready?

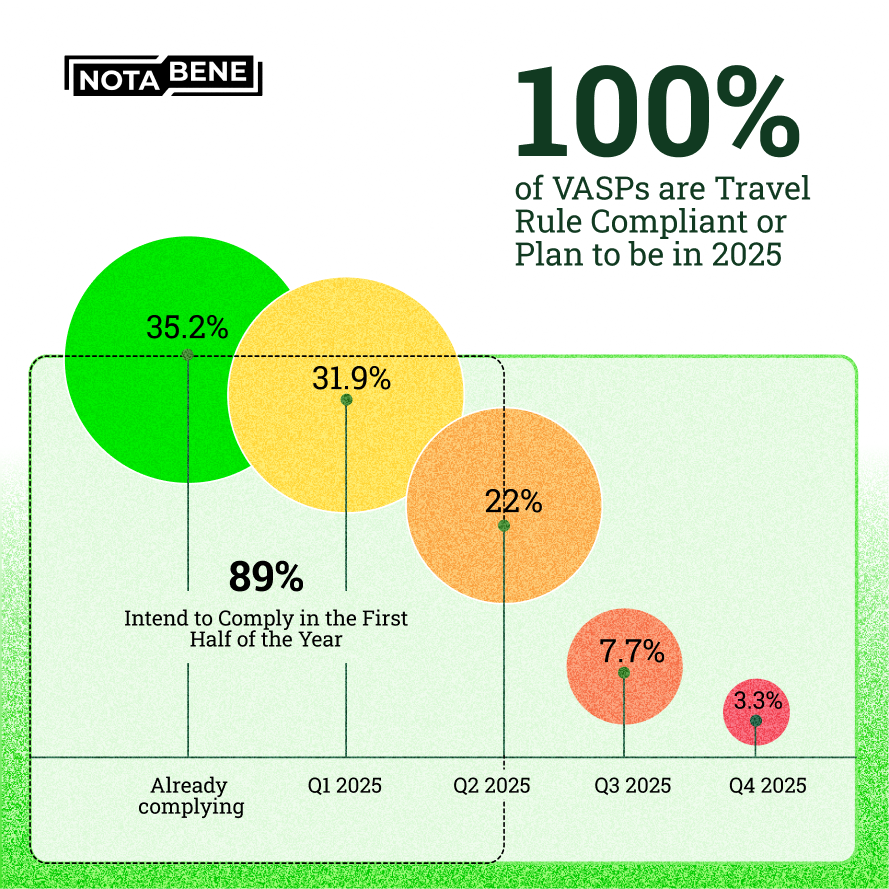

In April 2025, Notabene released the State of Crypto Travel Rule 2025 Report, the fourth annual edition of our comprehensive analysis of Travel Rule adoption, readiness, and implementation trends across the digital asset ecosystem. The report draws on survey data from nearly one hundred Virtual Asset Service Providers and input from regulatory bodies to capture how the industry is navigating evolving compliance landscapes.

One finding stood out. An unprecedented 100% of VASPs surveyed reported that they plan to be Travel Rule compliant by the end of 2025, reflecting a decisive shift from earlier years when compliance was optional or aspirational. Nearly nine in ten respondents expected to meet requirements in the first half of the year, underscoring the urgency across the market.

What the survey data shows is reinforced, and in many cases surpassed, by what we see across the Notabene platform itself. Over the past year, there has been a sharp increase in due diligence questionnaire requests, rapid adoption of policy engines, and a growing density of live connections between institutions. These are not theoretical commitments. They are operational signals that firms are actively raising their compliance standards to work with one another.

The data also revealed deeper operational change. Institutions are increasingly blocking withdrawals until beneficiary information is confirmed and returning deposits if originator data is missing. Compliance is no longer a policy exercise. It is becoming embedded directly into transaction flows, counterparty selection, and go to market decisions.

Taken together, the message is clear. Travel Rule compliance is no longer a regulatory checkbox. Companies operating on the Notabene platform are setting a global standard for what good looks like, proving that robust compliance has become a prerequisite for participation, connectivity, and growth in an increasingly interconnected and regulated digital asset economy.

Open messaging layers are essential for global stablecoin payment networks

Stablecoins will only deliver on truly global, borderless payments if the messaging layer is open. We’ve seen this before: shared standards like SWIFT and ISO 20022 made global bank-to-bank transactions possible, just as HTTP, SMTP, and SSL allowed the open internet to scale beyond closed, proprietary networks.

The same is true for crypto. Travel Rule compliance and transaction authorization cannot rely on closed protocols controlled by a few players. That approach fragments the ecosystem and limits innovation.

This is why we built the Transaction Authorization Protocol (TAP). TAP is an open messaging standard that enables pre-settlement coordination while preserving the permissionless nature of blockchain networks. It adds the missing authorization layer so transactions carry intent, compliance, and accountability alongside value.

By embedding regulatory checks directly into transaction flows, TAP turns compliance into infrastructure. Stablecoin payments become faster, safer, and more interoperable than traditional rails.Backed by Notabene’s open network of 2,000+ institutions, TAP lays the foundation for mainstream, compliant global stablecoin adoption.

Policy, payments, and infrastructure are converging

Trust is not built by infrastructure alone. It is reinforced through community. Our community-building initiatives in 2025 helped to generate a shared understanding, open dialogue, and alignment across the crypto payments ecosystem.

At our second annual Notabene Summit in New York City, we convened leaders from financial institutions, crypto-native companies, regulators, and infrastructure providers as stablecoins and compliant payments moved from theory to execution. The Summit focused on the convergence of traditional finance and crypto, the role of stablecoins in cross-border payments, and the importance of industry-regulator collaboration as adoption accelerates.

The event also marked a major milestone for Notabene with the launch of Notabene Flow, opening a new chapter in compliant stablecoin payments. Panels featured senior leaders from organizations including Mastercard, Robinhood, the U.S. Treasury, the Blockchain Association, BVNK, and Bitso, with discussions centered on real-world execution: operationalizing stablecoin payments, navigating regulatory expectations, and building interoperable infrastructure that can scale globally.

We carried these conversations forward with Stack Chats, a video interview series focused on the strategic and operational realities of payments, compliance, and digital asset infrastructure. Episodes featured leaders including Clarisse Hagege, Anoosh Arevshatian, and Kevin Lehtiniitty, sharing candid perspectives on innovation, regulation, and global scale.

The next episode will launch in early 2026 as these conversations continue into the year ahead.

Looking Ahead to 2026: From Momentum to Execution

The foundation we laid in 2025 sets a clear direction for the year ahead and we could not be more excited to execute our vision for an open, trusted, and value-accruing network of regulated financial institutions.

We’re focused on the following areas as we hit the ground running in 2026.

Building the system of record for regulated financial institutions

As large financial institutions and regulated crypto exchanges continue to build and grow in additional jurisdictions across the globe, they demand a best-in-class authorization and orchestration layer to power their transactions in a compliant and trusted way.

In the United States, proposed legislation such as the GENIUS Act reflects a broader shift toward clear, enforceable expectations for digital asset transactions. While regulatory frameworks differ by jurisdiction, the direction is consistent: regulated institutions need infrastructure that can support authorization, compliance, and reporting by default. This continued alignment reinforces the need for a shared system of record as digital assets move further into mainstream financial activity.

With our powerful set of tooling that facilitates automated decision-making and compliance engine with unmatched straight-through processing rates, we are fast becoming the de facto system of record for FIs, fintechs, and crypto-natives as they build out their payments infrastructure. Our commitment to open standards, interoperability, and industry-leading security have made Notabene the first name that regulated institutions turn to for compliant, trusted digital asset transactions.

Combined with automated reporting and analytics, our powerful transaction authorization platform has evolved beyond so much more than a Travel Rule compliance solution. Our customers are now turning to us as a foundational piece of their core digital asset infrastructure—and we're doubling down on our investment in product innovation to help our customers drive even more efficiency and compliant transaction volume on their platforms while de-risking their business at the same time. You can expect many more product enhancements on our core platform in 2026 to drive even more value for our customers.

Enabling high-value B2B stablecoin payment flows across the globe

As we write about in our Notabene Flow whitepaper, there is a good reason that stablecoins have yet to take a meaningful bite out of the $120T global B2B payments market. Context is missing. Trust is missing. Authorization is missing. While the gains in transaction speed and affordability are undeniable for a classic one-directional push payment, the reality is that the higher-value payments that unlock real utility for large enterprise need to have Trust, Context, and Authorization in place to enable payment types that they rely on for daily commerce, pull payments and recurring subscriptions, and metered billing.

This is where the Notabene Flow vision meets reality. By bringing this payment layer to our existing network of active regulated FIs and exchanges, Notabene is set to kickstart the adoption of stablecoins for B2B payment applications in 2026. We’re thrilled to be working side-by-side with our founding partners of Notabene Flow to continue building out our APIs and tooling to support their business use cases and many more as the year unfolds.

You can sign up today to join the network, and join us in-person in New York and London to learn more at our Notabene Flow Roadshow meetups next month.

Accelerating the agentic payments future

Perhaps the only word more ubiquitous than stablecoins last year was agentic. And for good reason, with agentic payments poised to revolutionize the way that consumers and businesses operate in 2026 and beyond. Notabene is actively investing in building this future with some exciting new developments in our Transact product, bringing robust and instantaneous counterparty due diligence to our 250+ customers, as well as working to bring more complex payment routing to members of the Notabene Flow network with real-time payment orchestration built not only on efficient routing but also factoring in the critical elements of counterparty trust and transaction context so that agentic payments can really prioritize what matters most to each individual party.

Keep an eye on this space as we invest in accelerating the future of agentic payments for our customers in 2026.

Thank you for building with us in 2025. Here’s to an even more incredible 2026!

To our customers, partners, and community, thank you for being a part of the Notabene ecosystem in 2025. A core part of our philosophy is the belief that no one company alone can build the future we all want to see. We thank you for being a part of our story in 2025 and are honored for you to join us as we move forward in 2026 with clarity of vision and a commitment to building real value for businesses across the globe.

2025 was the year trust became infrastructure.

2026 will be the year we scale it into everyday global payments.

Join us as we continue building the trust layer for global money movement.

Anastasiia from the Notabene product team walks through an example of a pull transaction on Notabene Flow. This demo shows the full end-to-end flow, with Travel Rule compliance and transaction authorization built-in to every payment on the Flow network.

To learn more, schedule a custom demo with the team or read our introduction to Notabene Flow developer documentation at devx.notabene.id.

This morning at the Blockchain Association's Policy Summit, Senator Cynthia Lummis dropped significant news: the Senate's bipartisan market structure draft will be released by the end of this week, with markup planned for next week.

With the GENIUS Act now law and its rule-making process underway, Washington has turned its attention to the fundamental question that's been hanging over the industry: who regulates what in crypto?

The answer matters because it determines whether the SEC or CFTC has jurisdiction, what registration requirements apply, and ultimately how digital asset markets can operate in the United States.

After months of negotiations between Senate Banking and Agriculture Committees, the legislative framework that will determine how digital assets are regulated in the United States is finally ready for public review.

Timeline: How We Got Here & What Comes Next

Let’s quickly review how we got here. On July 17, 2025 Digital Asset Market Clarity Act of 2025 (CLARITY Act, now it has to pass the Senate, and after that it goes to the president to be signed into law.

- July 17, 2025: House passes CLARITY Act (H.R. 3633) with bipartisan support, 294-134

- November 10, 2025: Senate Agriculture Committee releases 155-page bipartisan discussion draft on digital commodities and CFTC oversight

- September-December 2025: Senate Banking Committee negotiates bipartisan draft covering SEC jurisdiction (not yet public)

- Last week: First bipartisan member meeting between Senate Democrats and Republicans

- Last night (Mon, Dec. 8): Democrats delivered final asks to Republican staff

- This week: Draft bill to be released by week's end

- Next week: Markup planned

- End of 2025: Senate Banking Chair Tim Scott's goal for committee votes on both bills

- Early 2026: Target for merged Senate floor vote

The Two-Committee Process

The Senate is taking a different approach than the House. Rather than the joint committee process used in the House, the Senate has two separate committees working in parallel.

The Senate Banking Committee handles SEC-facing aspects of market structure: how to define investment contracts, what qualifies as an ancillary asset, and related securities questions. Chair Tim Scott started with Republican-led discussion drafts, most recently the Responsible Financial Innovation Act of 2025, then worked to turn this into a bipartisan product through meetings with crypto-friendly Democrats and industry roundtables.

The Senate Agriculture Committee focuses on digital commodities and CFTC oversight. On November 10, Chair John Boozman and Senator Cory Booker released a 155-page bipartisan discussion draft that builds on the House CLARITY Act but takes a more prescriptive approach to customer protection. It includes tighter proprietary trading limits, detailed conflict-of-interest rules, enhanced retail protections, and would create an Office of the Digital Commodity Retail Advocate at the CFTC.

The two committees communicate extensively to ensure their bills work together, even though they're moving on separate tracks. Once both bills pass committee, they'll be stitched together on the Senate floor as a two-committee product.

Why This Week Matters

The timing is deliberate. With fewer than 10 legislative days left in 2025, Senate leadership wants to move quickly. According to Lummis, their staffs are exhausted after working through weekends and late nights, and it's time to reveal the product, give everyone a chance to review it over the holiday break, and move forward.

The first bipartisan member meeting happened last week and went well. Democrats delivered their final asks to Republican staff last night. Today, Gillibrand, Lummis, and other key senators are meeting to work through remaining issues.

"Industry is getting a little concerned about what's happening behind closed doors," Lummis said. “Our staffs are exhausted. I'm worried about the temperature and the flare, and it's just time to reveal a product."

Both senators were direct: when the draft drops, industry will be on a tight timeline to read it, vet it, and provide feedback. This is prime time for getting this done.

What Makes the Senate Bill Different

The Senate bill tackles issues the House CLARITY Act didn't address. According to Gillibrand, the House didn't have time to bring Democratic negotiators in to add their contributions, so while the House bill was bipartisan in vote count (294-134 in July), it was largely drafted by Republicans.

The Senate version includes substantial new provisions on decentralized finance exchanges and illicit finance. The Agriculture Committee draft explicitly left sections on DeFi and anti-money laundering incomplete, with bracketed language marking areas still under negotiation. These aren't just placeholders. They represent some of the hardest policy questions Congress has to answer.