BLOG

Insights on building trust infrastructure for global money movement

On November 10, 2025, the Banco Central do Brasil (BCB) published three major resolutions — 519, 520, and 521 — establishing a comprehensive regulatory framework for virtual asset service providers (VASPs), officially termed “sociedades prestadoras de serviços de ativos virtuais” (SPSAVs).

This marks a historic milestone in Brazil’s journey toward implementing Law No. 14,478/2022, the country’s legal foundation for virtual assets, and positions Brazil among the most advanced jurisdictions in Latin America in providing legal certainty on how digital asset service providers can operate.

Scope of the New Resolutions

- Resolution 519/2025 – This resolution defines the authorization process for SPSVAs. It clarifies how entities must apply for approval by the BCB before engaging in virtual-asset services.

- Resolution 520/2025 – This key regulation governs how SPSVAs and other authorised institutions can operate within Brazil’s virtual-asset market. It covers the types of services, governance, risk management, anti-money-laundering (AML) and counter-terrorist-financing (CTF) obligations (including Travel Rule requirements), and transition provisions.

- Resolution 521/2025 – This resolution integrates virtual-asset activities into Brazil’s foreign-exchange (FX) regime. It recognizes operations such as cross-border payments, stablecoin transactions and transfers involving self-hosted wallets as falling under the FX regulatory framework in Brazil.

Who Can Operate in Brazil’s Virtual Asset Market?

1. Sociedades Prestadoras de Serviços de Ativos Virtuais (SPSAVs)

Under Article 4 of Resolution 520, SPSAVs must be authorized by the BCB and may be classified as:

- Virtual Asset Intermediaries — Entities facilitating the purchase, sale, exchange, and management of virtual assets, including staking and FX-related operations.

- Virtual Asset Custodians — Entities responsible for safeguarding assets and private keys, maintaining records, and executing client instructions.

- Virtual Asset Brokers — Entities performing both intermediary and custodial functions.

2. Eligible Authorized Financial Institutions

The following already-regulated financial institutions may also offer virtual asset services, provided they formally notify the BCB in accordance with the established procedures:

- Commercial, investment, and “bancos multiplos”, as well as Caixa Econômica Federal.

- Securities brokers, distributors, and foreign exchange dealers.

These are henceforth referred to as eligible authorized institutions.

Transition and Grandfathering: Preparing for Compliance

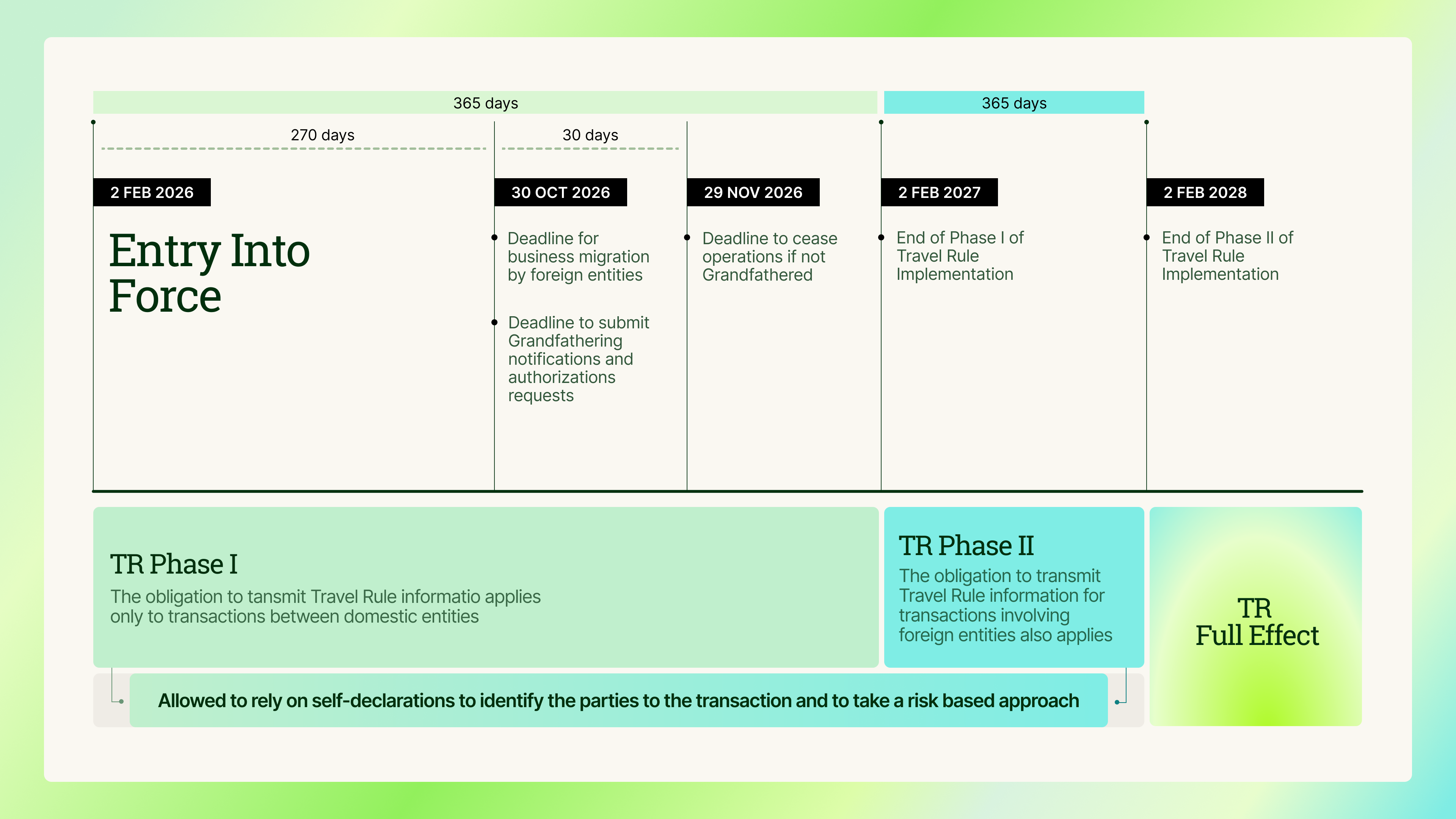

Institutions currently offering virtual asset services in Brazil must transition into the new regulatory regime established by the BCB. To ensure business continuity, the framework allows these entities to continue operating provided that they meet the following obligations by October 30, 2026 (270 days from the entry into force of Resolution 520 on February 2, 2026):

- Eligible authorized institutions (e.g., banks, brokers, distributors) must notify the BCB of their intent to continue providing virtual asset services.

- Other institutions currently providing virtual asset services must apply for authorization from the BCB to operate as SPSAVs.

- Foreign institutions offering virtual asset services to Brazilian clients must migrate their operations and customer base to either:(i) an eligible authorized institution, or

- (ii) an SPSAV already operating or established to carry out these activities.

To benefit from the grandfathering period, institutions must have already been offering virtual asset services before February 2, 2026.

After October 30, 2026, any institution that has not complied with the transition requirements will no longer be permitted to operate in Brazil’s virtual asset market and must cease operations within 30 days.

Finally, it is worth noting that Article 88 of Resolution 520 establishes an adjustment period between February 2, 2026 and the BCB’s decision on phase 1 of the authorization process, during which SPSVAs must demonstrate compliance with a defined set of obligations. These include:

- Implementing a risk-management framework covering market, credit (where applicable), operational, and liquidity risks.

- Maintaining a cybersecurity policy, an incident-response and action plan, and appropriate data processing, storage, and cloud-computing arrangements.

- Establishing internal controls to prevent the use of the Brazilian Financial System and Payment System for money laundering or asset-concealment crimes.

- Implementing procedures to comply with Law 13,810/2019 regarding UN Security Council sanctions.

- Adopting the accounting and audit standards applicable to financial institutions authorized by the Central Bank of Brazil.

- Complying with any additional requirements expressly imposed by regulation for institutions in the adjustment phase.

Once the aforementioned adjustment period has ended, SPSVAs must fully comply with the provisions of Law No. 14,478 of December 21, 2022, and with the regulations issued by the Central Bank of Brazil, even if no final decision has yet been made regarding their authorization request.

Travel Rule Implementation: Timeline and Requirements

Under Article 44 of Resolution 520, SPSAVs must comply with AML/CTF obligations and the Travel Rule, ensuring that identifying information accompanies virtual asset transfers.

Requirements

For each transfer, the originator’s institution must transmit data on both the originator and the beneficiary, as follows:

.png)

The resolution explicitly establishes the obligation to report suspicious activities and to notify the BCB of any difficulties in complying with the Travel Rule that stem from the practices adopted by counterparties authorized by the BCB.

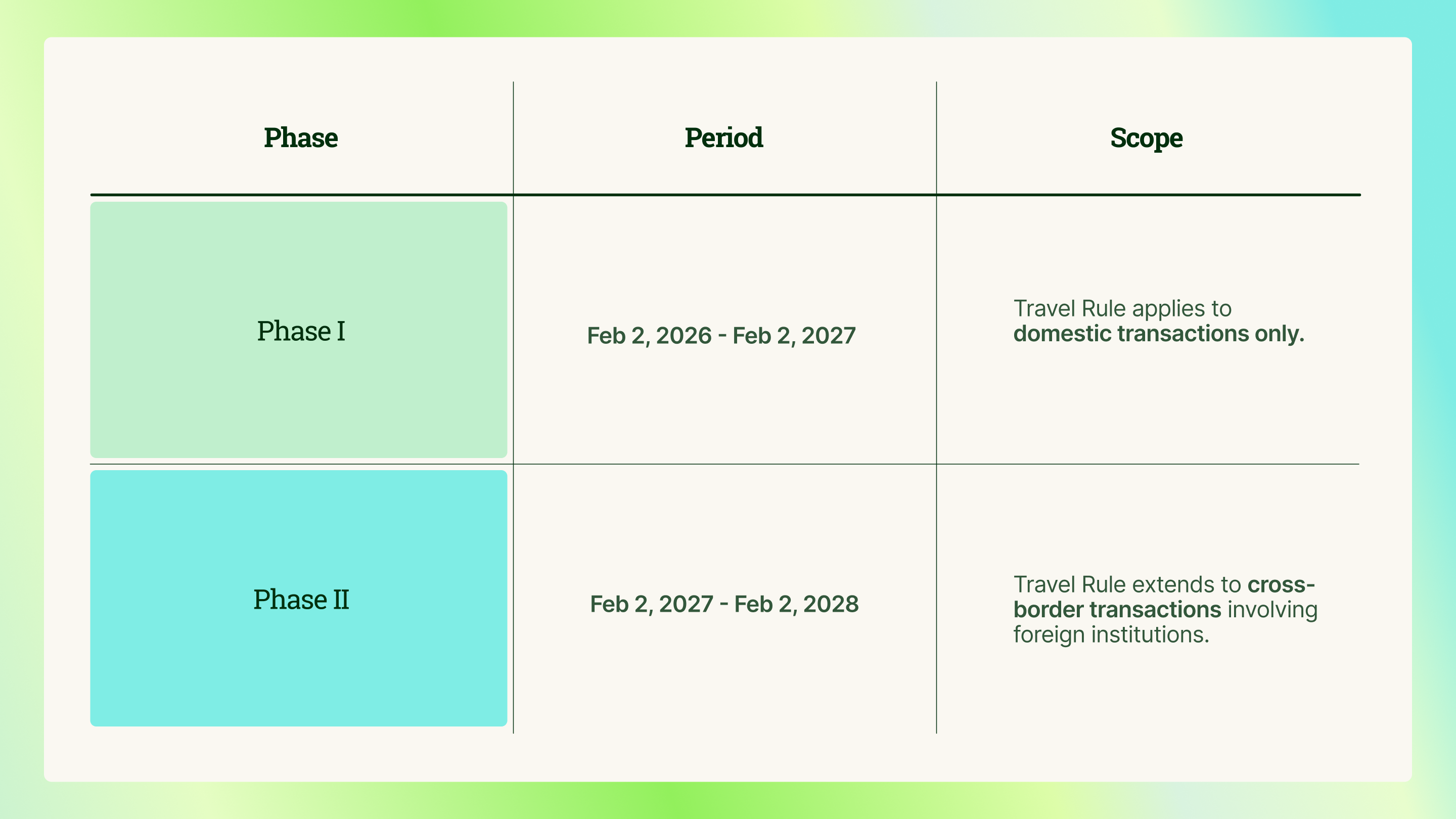

Two-Year Phased Implementation

Travel Rule implementation will occur in two stages between 2026 and 2028, according to Article 89 of Resolution 520:

During both phases, SPSAVs may rely on self-declarations from clients to identify the transacting parties and the purposes of the transactions, provided these are documented and accessible to the BCB.

Full compliance will be mandatory starting February 2, 2028.

The illustration below provides an overview of the grandfathering timeline and the phased implementation schedule for Travel Rule requirements.

Self-Hosted Wallets and FX Integration

Resolution 521 defines self-hosted wallets (“carteiras autocustodiadas”) as wallets where the user controls the private keys without a third-party intermediary.

Under the resolution, the provision of services that include transfer to or from a self-hosted wallet is subject to Brazil’s foreign exchange (FX) framework, and SPSAVs are required to identify the wallet owner.

Key Takeaways

- Brazil’s Central Bank (BCB) is assuming full regulatory responsibility for the country’s virtual asset ecosystem, establishing clear rules for authorization, operation, and supervision.

- A grandfathering period allows existing providers to continue operating compliantly, provided they meet the notification and authorization requirements outlined in the resolutions by October 30, 2026.

- The two-year phased rollout of Travel Rule obligations offers the industry a measured timeline to adapt systems, processes, and counterpart relationships to the new compliance expectations.

- The requirement to identify self-hosted wallet owners under the foreign exchange (FX) regime represents a move toward comprehensive transaction traceability across the digital asset ecosystem.

- By implementing these measures, Brazil aligns its framework with global AML and Travel Rule standards, setting a regional benchmark for regulatory modernization in Latin America.

Prepare your business for Brazil’s new Travel Rule requirements.

Notabene helps virtual asset service providers automate compliance, exchange Travel Rule data securely, and stay aligned with local and global regulations.

👉 Register for our upcoming webinar: How to Prepare for Brazil’s New Crypto Regulatory Framework if you operate in Brazil or support customers who do. This session will help you understand what’s changing and what comes next.

Stack Chats Episode 3: The Future of Payments and the Rise of Money 3.0

In this episode of Stack Chats, Notabene CEO Pelle Braendgaard sits down with Kevin Lehtiniitty, CEO of Borderless.xyz, to explore how stablecoins are evolving from speculative assets into functional payment infrastructure. Kevin shares insights on building the foundational rails that connect global stablecoin networks to local financial systems, unlocking seamless interoperability and real-world utility. Watch the full episode below:

From the limitations of traditional cross-border payments to the promise of “Money 3.0,” this conversation dives deep into how Borderless is making stablecoin adoption practical—and compliant—for fintechs, wallets, and regulated entities.

📌 Topics include:

- Bridging stablecoin networks with local payment systems

- Regulatory interoperability and compliance-by-design

- What “Money 3.0” means for the future of finance

- Building for developers and scaling across jurisdictions

Pelle and Kevin set the stage by looking at where stablecoins fit into today’s financial landscape and why so many companies are turning to them as part of their core infrastructure. Their conversation moves from the challenges businesses face today to the emerging solutions shaping the next generation of payments. What follows is a look at the key themes they explored and why they matter for anyone building or using stablecoin-based systems. Read on for a breakdown of the rest of the discussion points:

Why global payments still feel local

Once the conversation begins, one theme emerges right away. Even though stablecoins let value move across the world as easily as sending an email, the financial systems around them remain deeply local. Stablecoins operate on global, always-on networks. But banks, licensing regimes and national currencies still function in country-by-country silos.

Kevin has watched this play out throughout his years in the industry. Whether working on issuance, custody, collateral or payments, the same challenge appears: as soon as stablecoins touch the real world, companies encounter a maze of regulatory requirements, fragmented liquidity and inconsistent banking access.

This is the problem Borderless.xyz set out to solve. Rather than becoming another regional on or off ramp, Borderless focuses on the connective layer between them. A single integration gives companies access to diverse liquidity providers, payment partners and banking channels across many markets. Instead of every business rebuilding the same integrations repeatedly, Borderless abstracts that work into one unified network.

The hidden cost of pre-funding in global money movement

A major theme Pelle and Kevin explore is the role of pre-funding in today’s payments ecosystem. For most cross-border flows, especially in emerging markets, companies must lock funds in multiple partner accounts to simulate real-time settlement.

This creates several issues:

- Large amounts of capital sit idle across bank accounts in many countries.

- That capital is exposed to local banking risk.

- Treasury teams face constant operational pressure to balance and rebalance accounts.

Kevin shares examples of remittance companies holding more than four hundred million dollars in pre-funded balances simply to keep corridors running. This cost ultimately flows to end users through fees.

Stablecoins change the equation. Because they can move globally in near real time, they allow companies to:

- Reduce pre-funding from days of coverage to a few hours.

- Move liquidity around the clock, including weekends and holidays.

- Unlock capital that can go back into product, growth or customer acquisition.

Businesses do not have to overhaul their existing treasury workflows to gain these benefits. Stablecoins simply let them operate with far more flexibility and lower capital cost.

Open networks outpace closed loops

As the discussion evolves, Pelle and Kevin look closely at the difference between closed loop payment networks and open ones. Closed networks are controlled by a single company that determines participation and flow. They can work in limited contexts, but their total value is capped by the value of the operator controlling them.

Open networks grow far larger because value is created by everyone participating, not just the administrator. Kevin highlights several historical examples:

- The shift from isolated charge-card programs to the Visa consortium.

- The standardization of rail gauges that unlocked interstate commerce.

- The rise of Linux as the foundation of cloud computing and modern devices.

Stablecoins and public blockchains follow the same pattern. They create shared standards that many companies can build on, which expands use cases far beyond what any one entity could design.

Notabene takes the same approach. Its Transact product is built on TAP, an open messaging protocol that supports different transaction types and authorization flows without locking users into a closed database or proprietary environment. This keeps innovation open to the entire ecosystem while providing strong compliance controls.

Moving stablecoins from simple transfers to real business workflows

Most stablecoin payments today are push-only. Tokens sit in a wallet and move only when someone signs a transaction. This works for one-time transfers, but not for the full range of business payments the world runs on.

Traditional payments rely heavily on pull flows, such as:

- Subscriptions and recurring billing.

- Invoicing and accounts receivable versus accounts payable processes.

- Automated treasury and liquidity management.

- Merchant settlement and reconciliation.

Card networks became central to commerce not only because they moved money, but because they integrated directly into business systems and workflows.

This is the missing capability in stablecoin-based payments today. It is also where the partnership between Borderless.xyz and Notabene becomes important.

By combining:

- Borderless’s connectivity to stablecoin and fiat liquidity in more than seventy countries.

- Notabene’s open messaging and compliance layer built on TAP.

They are bringing stablecoin pull payments, treasury automation and workflow connectivity to businesses that want to move beyond one-off transfers. The result is a stablecoin infrastructure layer that mirrors how businesses already operate, while taking advantage of global, always-on settlement.

Money 1.0, Money 2.0 and the arrival of Money 3.0

Kevin introduces a simple framework for understanding how global money movement has evolved.

Money 1.0

Traditional networks like Swift and card schemes created the first generation of cross-border connectivity. These systems were built before the internet era. Settlement is slow, fragmented and expensive.

Money 2.0

Fintech companies improved the experience but did not change the underlying rails. To cover the limitations, they added layers of pre-funding, user-friendly interfaces and workflow tools. This produced many successful companies but did not solve the core infrastructure challenges.

Money 3.0

With blockchains and stablecoins, payments can finally be modernized at the foundation. Instead of adding more band-aids, value can move directly between counterparties that support the same stablecoin and blockchain network. This removes unnecessary intermediaries and supports real-time global settlement.

Pelle and Kevin argue that the next five to ten years will determine whether global payments continue relying on legacy patches or shift decisively to this new model.

What the next decade could look like

As stablecoin adoption accelerates across remittance providers, PSPs and global businesses, the need for an open, infrastructure-ready payments layer becomes clearer. The vision that Notabene and Borderless share is grounded in a few core ideas:

- Stablecoins can settle business payments directly.

- Local liquidity can be accessed without each company rebuilding the same integrations.

- Workflows and compliance can run on open messaging networks like TAP.

- Money can finally move at the speed of the internet rather than the speed of legacy rails.

For businesses exploring stablecoins, this episode offers a practical look at what it takes to move from experimentation to production. Money 3.0 is not a distant idea. It is already taking shape, and the companies building it are laying the groundwork today.

Episode breakdown

Here is a quick minute-by-minute guide to the conversation:

- 00:00 - 03:00

- Introductions. Pelle and Kevin talk about their history in stablecoins and why stablecoin adoption has felt like "it is coming next year" for nearly a decade.

- 03:00 - 08:00

- Global assets vs local fragmentation. Why regulatory licenses, banking rails and central bank currencies will always remain local, and what that means for anyone building on stablecoins.

- 08:00 - 15:00

- On and off ramps as the next generation of banks. Borderless’ view of orchestrators, market makers and local liquidity partners, and why building the same integrations again and again adds no real enterprise value.

- 15:00 - 22:00

- Where stablecoins deliver the most value today. Dollarization and the "store of value" use case in emerging markets versus the much bigger opportunity in global payments.

- 22:00 - 30:00

- Pre-funding and the illusion of real-time. How correspondent banking actually works, the risks of pre-funding in different markets and why stablecoins can release hundreds of millions in trapped capital.

- 30:00 - 36:00

- Open networks vs closed loops. Visa, railroads and Linux as case studies for why open systems outcompete walled gardens over time, and what that means for stablecoin ecosystems.

- 36:00 - 42:00

- TAP, open messaging and Flow / Flow Forward. How Notabene uses an open protocol rather than a closed database, and how that supports many use cases from payments to trade settlement on the same compliance rails.

- 42:00 - end

- Money 1.0, 2.0 and 3.0. Kevin’s framework for the future of money, and how Borderless XYZ and Notabene think about success over a 5 to 10 year horizon.

🎙️ Stack Chats is Notabene’s video series for product leaders, fintech builders, and infrastructure innovators shaping the next generation of blockchain-based payments.

We are standing at the edge of a defining opportunity for the crypto industry. The Travel Rule is still perceived by many as a burdensome obligation that should be met with a check-the-box approach. But in reality, it is the catalyst for building critical infrastructure needed to unlock stablecoin payments at global scale and connect digital assets to the real economy. Once it is understood in this light - not as another compliance obligation, but as the foundation of the next phase of market infrastructure - its effective implementation becomes a strategic imperative deserving of united industry action. Only collective alignment around interoperability and openness will make effective implementation possible.

The Value of the Travel Rule: A Catalyst for Real-World Adoption

The Travel Rule requires financial institutions to securely exchange originator and beneficiary information before or in parallel with a virtual asset transfer. At first glance, this might seem like a regulatory nuisance, another box to check. In reality, it introduces a profound change in how crypto transactions work.

Natively, crypto payments are unilateral and context-free: senders can move value without the receiver’s consent, and the information recorded on the blockchain provides no information about who was transacting or why. These characteristics have slowed down the adoption of crypto rails for business and institutional use cases that depend on context, authorization, and risk controls.

The Travel Rule changes that. By requiring counterparties to exchange information before settlement, it introduces, for the first time, an opportunity to build a pre-transaction authorization flow into crypto transactions. Institutions must communicate before funds move. This creates the missing messaging layer that connects transactions to compliance processes, payment context, and counterparties.

What began as a regulatory requirement has become a forcing function for the infrastructural upgrade that crypto has been missing. Through the Travel Rule, the industry is building the same kind of pre-settlement messaging rails that power traditional payments, where transactions carry context, receivers can approve or reject transfers, and value and information travel together.

In this sense, the Travel Rule is more than a compliance requirement - it serves as the catalyst for building the missing foundations of institutional trust in crypto. By requiring institutions to exchange information before settlement, it opens the door to systems that restore control and risk management to both sides of a transaction. By mandating data exchange, it attaches real-world context to payments. And by making counterparties visible, it creates a trust fabric that allows institutions to confidently transact with third-parties in open loop systems, opening up business opportunities.

Together, these shifts establish the trust layer that crypto has been missing and unlock its potential to move beyond speculative markets and power the next generation of global payment systems.

Why Travel Rule Implementation Has Stalled

Since its adoption by the FATF in 2019, the Travel Rule has been implemented as a regulatory requirement for virtual asset transactions across jurisdictions worldwide. The FATF reports that 99 jurisdictions have passed or are in the process of passing Travel Rule legislation¹. Regulatory clarity is no longer the barrier. The barrier is infrastructure and whether the industry will choose a future defined by open connectivity, or fragmentation and control.

From the outset, interoperability has been cited as a primary barrier to Travel Rule implementation. In hindsight, this was almost inevitable.

Travel Rule information pipelines are emerging as the financial messaging backbone of the crypto economy. In traditional finance, we have clear precedents: SWIFT is classified as a systemically important messaging network deserving of cooperative oversight by G10 central banks, the European Central Bank, and the chair of the G10 Committee on Payment and Settlement Systems². Control over the Travel Rule messaging layer is highly attractive as it ultimately provides control over market access. Thus far, the fight for control has come at the expense of effective Travel Rule implementation, with limited coordination toward establishing open standards or interoperability.

As a result:

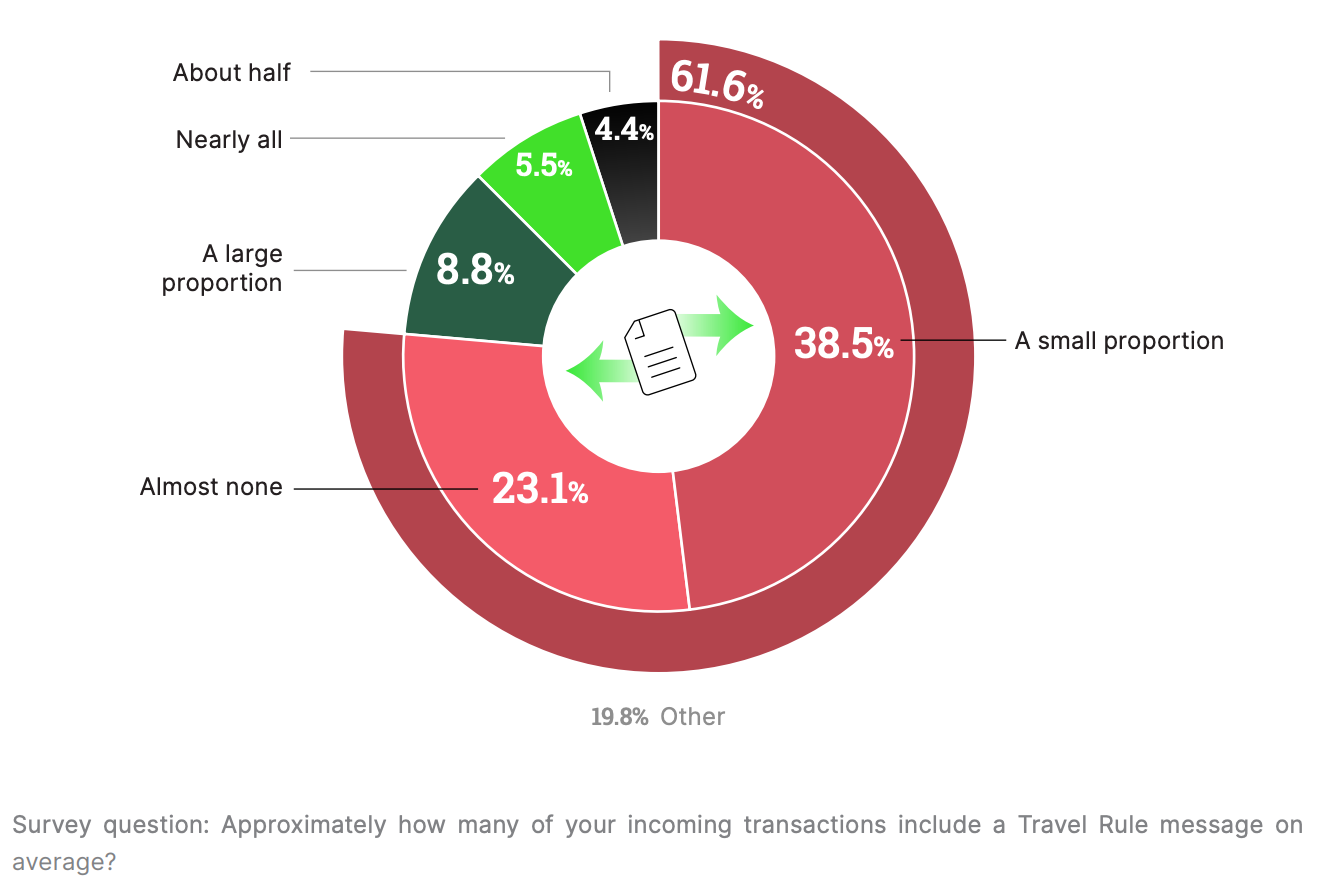

- Compliance silos persist, reflecting not just the lack of interoperability and open standards, but also the fragmented pace of Travel Rule adoption and enforcement worldwide. According to the 2025 State of Crypto Travel Rule survey, over 60% of respondents reported that almost none or only a small portion of incoming transactions include the required Travel Rule information

- Law enforcement lacks access to critical information, limiting the ability to investigate and disrupt illicit activity

- Crypto cannot fulfill its potential because it lacks the infrastructure necessary for integration into the global economy, as further explained in the above section

A Moment of Choice: Network Effects or Network Control

Overcoming the challenges in Travel Rule adoption is not simply about regulatory compliance; it is about unlocking crypto’s role as the next-generation backbone of global finance.

The core promise of crypto lies in openness: borderless settlement and universal reach. These advantages are only realized if the supporting messaging layer is equally open. Just as the internet scaled through universal protocols rather than private networks, crypto adoption can only reach its potential through open standards.

History has already shown that open networks win:

- SWIFT and ISO 20022 created a shared messaging language that enables thousands of financial institutions to transact globally.

- HTTP for web browsing, SMTP for email, and critically, SSL for secure transactions allowed any computer to connect to any other, regardless of service provider, enabling the open web to flourish and creating exponentially more value than the closed systems they replaced.

Crypto must follow this path. The messaging layer for Travel Rule compliance and transaction authorization cannot be proprietary and controlled by a handful of market actors. It must be built on open standards that allow every institution to connect, transact, and innovate without seeking permission from a competitor. Closed, proprietary protocols create fragmentation, entrench market power, and suppress innovation, preventing crypto from fulfilling its economic potential.

Advantages of Open Standards

Innovation through competition

Open networks eliminate lock-in. Institutions can choose service providers freely without risking access to counterparties. This forces innovation to flourish as providers must compete on service quality, not network control.

Connectivity over control

Open, neutral messaging standards ensure every institution retains autonomy over counterparties, risk rules, and transaction authorization, without ceding control to a central operator. An open messaging layer also creates the network effects that allow the industry to prosper. Every new participant increases the value of the network for all others.

The Cost of Fragmentation

The alternative is a fragmented ecosystem that undermines the value-add of crypto. Imagine if, instead of a unified network like SWIFT, the global financial system had evolved into dozens of incompatible, closed messaging networks, each unable to communicate with the others. Payments would stall at borders, institutions would struggle to reach counterparties, and innovation would be stifled by inefficiency. This is precisely the path crypto risks taking without open standards. Competing silos may deliver short-term advantages to a few, but they erode the collective value for all. For a technology built on openness and global connectivity, allowing fragmentation to persist would mean falling short of its original promise. Without interoperability, crypto cannot fulfill its potential as a truly borderless financial system, and we risk setting the industry back by years.

A Call to the Industry

If the Travel Rule messaging layer is built on proprietary networks, the industry will remain trapped in compliance silos. Travel Rule will become a regulatory burden that slows down business, instead of a catalyst to build the infrastructural upgrade that crypto has been missing.

But if we embrace open standards, we can turn Travel Rule into an opportunity to adopt an open authorization and messaging layer that connects counterparties, unlocks network effects and powers real-world adoption.

Solving Travel Rule interoperability is not only a compliance urgency, it is a strategic imperative for the industry to flourish. And it requires a collective endorsement of open standards.

Notabene is committed to an open and interoperable future. Our platform is powered by the Transaction Authorization Protocol (TAP), an open standard purpose-built for transaction authorization and Travel Rule compliance in digital assets. We invite all industry participants, regulators, and innovators to join us in advancing this standard, and we reaffirm our commitment to ensuring full interoperability with other open standards that share our vision for a connected and transparent digital finance ecosystem.

¹ FATF, June 2025, VIRTUAL ASSETS: TARGETED UPDATE ON IMPLEMENTATION OF THE FATF STANDARDS, Figure 1.11.

Few technologies have captured the imagination of the financial world quite like stablecoins. They promise to make money programmable, borderless, and instant. With blockchain as their foundation, stablecoins can streamline settlement, reduce costs, and open up a new era of global commerce.

Yet despite their growing adoption, stablecoins represent only 0.03% of the $120 trillion B2B payments market. The reason is simple: on their own, stablecoins don’t constitute a full payment system.

Businesses need more than fast transfers. They need context—the ability to link payments to contracts, invoices, and compliance data. Institutions processing payments for businesses also need to operate with counterparty trust and robust compliance frameworks.

The potential of stablecoins to revolutionize payments will remain largely untapped until these missing layers are built.

Why Stablecoin Payments Need Authorization and Context

Traditional payment systems have long relied on authorization—the ability to approve a transaction before settlement. When a card is swiped or a wire is initiated, institutions verify funds, screen for fraud, and apply compliance checks. This two-step process—authorization first, settlement later—is what makes payments reliable, reversible when needed, and compliant.

Equally important is the context: the information that moves alongside the funds. Payment messages transmit essential information for compliance and business operations, including Travel Rule data, invoice numbers, merchant details, and customer identifiers. This context allows businesses to reconcile payments with contracts, match them with invoices, and meet AML/CTF requirements.

Crypto transactions, by contrast, are unilateral and lack context. Whoever holds the private keys decides has full control to decide whether settlement happens. Without a pre-transaction authorization step or counterparty context, institutions have no way to vet, approve, or refuse incoming funds. Additionally, blockchains record only the amount, asset, and wallet addresses—no information about the counterparty, purpose, or which invoice it references.

Without a pre-transaction authorization step or counterparty context, crypto rails can’t power real-world payments. Businesses need to know who they’re transacting with, why a payment is being made, and whether it meets compliance criteria before funds move.

This is a key limitation stablecoins face today. They enable instant, global value transfer, but lack the context, trust signals, and institutional coordination that make payments truly work for businesses.

How the FATF Travel Rule Became a Catalyst for Crypto Authorization

When the FATF introduced the Travel Rule in 2019, it created the perfect conditions to build a compliant authorization layer for crypto. The rule requires counterparties in a virtual asset transaction to exchange originator and beneficiary information before settlement.

For the first time, crypto institutions were required to collaborate before a transaction occurred, mirroring the same pre-transaction authorization and due diligence flows that underpin traditional finance.

At Notabene, we saw this as a pivotal opportunity. The Travel Rule isn’t just a regulatory requirement—it’s an architectural upgrade. It gives the industry a shared standard to exchange trusted information, unlock counterparty confidence, and enable compliant, authorized crypto transactions at scale.

We’ve Already Built It: Pre-Transaction Authorization as Best Practice

Over the past five years, Notabene has turned Travel Rule compliance into an operational standard for the industry.

Today, more than 2,000 institutions across 100+ jurisdictions rely on Notabene’s open Transaction Authorization Protocol (TAP) to exchange verified transaction data and pre-transaction authorizations. To date, the Notabene Network has powered more than $1.5 trillion in compliant transaction volume.

Within our network, pre-transaction authorization has become an established best practice. Counterparties exchange compliance data, verify each other’s risk profiles, and explicitly approve transactions before funds move.

The Dilemma: Global Travel Rule Adoption Still Faces Gaps

Since the FATF introduced the Travel Rule in 2019, global implementation has expanded rapidly but unevenly.

According to the FATF’s June 2025 targeted review, 85 jurisdictions now enforce or have enacted Travel Rule legislation, up from 65 in 2024. 99 out of 117 jurisdictions had either passed or were in the process of passing relevant legislation at the time of the report.

However, only 35 jurisdictions have initiated active enforcement or supervisory actions. Nearly 60% of jurisdictions with legislation have yet to begin active Travel Rule enforcement.

Even where rules exist, VASPs face structural barriers to compliance. Because public blockchains are open settlement layers, VASPs cannot fully control the origin of incoming transfers. Many VASPs still lack the ability to reject deposits that arrive without verified Travel Rule data or from untrusted counterparties, which undermines their ability to maintain consistent counterparty risk controls.

This fragmented and inconsistent implementation, coupled with persistent technical interoperability challenges, limits the Travel Rule’s full potential. To unlock the next generation of payments, authorization and compliance must become built-in properties of the transaction, not optional layers added after the fact.

Notabene Flow: Stablecoin Payments with Authorization Built In

Enter Notabene Flow, the open stablecoin payments platform that makes authorization and Travel Rule compliance native to every payment.

Flow uses an addressless payments architecture: settlement addresses are revealed only after all Travel Rule information is exchanged and the required due diligence, consent, and compliance checks are completed. No address, no payment—and as a result, no possibility of unauthorized or non-compliant settlements.

Here’s how it works in a Pull Payment scenario:

- Payment initiation – The merchant’s payment service provider (PSP) issues an invoice and payment request in Flow, automatically generating a Travel Rule message that includes payee data and transaction details.

- Payment response – The payer selects their payment provider, who adds payer information to the Travel Rule record.

- Dual authorization – Both counterparties conduct compliance and risk checks.

- Settlement and disclosure – Once both counterparties have completed their compliance checks and authorized the transaction, the agent representing the payee sends an authorization message back to the agent representing the payer. This message includes the settlement address, which is revealed only at this stage. .

This model elevates pre-transaction authorization from a best practice to a built-in feature of every Flow payment. It also transforms the Travel Rule from an isolated compliance task into a requirement enforced by the design of the payment itself.

By revealing settlement addresses only after both sides complete authorization and exchange verified information, Flow makes it technically impossible to receive unvetted or non-compliant deposits. Institutions regain full control over inbound payment flows, strengthening their ability to apply consistent counterparty risk policies, prevent unwanted exposure, and enforce compliance at the protocol level.

Business-Ready Stablecoin Payments—Built for the Real World

Notabene Flow transforms stablecoins from fast settlement tools into a fully authorized, compliant, and business-ready payment network.

By combining the instant settlement of stablecoins with a pre-transaction authorization and compliance layer, Flow delivers what neither can achieve alone:

- Instant, borderless settlement without intermediaries

- Pre-transaction authorization, counterparty verification, and Travel Rule compliance

- End-to-end control and transparency across every transaction

With Flow, companies can finally unlock the efficiency of stablecoins — without sacrificing oversight, trust, or regulatory alignment.

This is the foundation for the future of B2B payments: instant, compliant, and ready for the real world.

Explore Notabene Flow and apply to become a Notabene Flow founding partner.

How Notabene Flow makes authorization and Travel Rule a built-in component of Stablecoin Payments

Few technologies have captured the imagination of the financial world quite like stablecoins. They promise to make money programmable, borderless, and instant. With blockchain as their foundation, stablecoins can streamline settlement, reduce costs, and open up a new era of global commerce.

Yet despite their growing adoption, stablecoins represent only 0.03% of the $120 trillion B2B payments market. The reason is simple: on their own, stablecoins don’t constitute a full payment system.

Businesses need more than fast transfers. They need context—the ability to link payments to contracts, invoices, and compliance data. Institutions processing payments for businesses also need to operate with counterparty trust and robust compliance frameworks.

The potential of stablecoins to revolutionize payments will remain largely untapped until these missing layers are built.

Why Stablecoin Payments Need Authorization and Context

Traditional payment systems have long relied on authorization—the ability to approve a transaction before settlement. When a card is swiped or a wire is initiated, institutions verify funds, screen for fraud, and apply compliance checks. This two-step process—authorization first, settlement later—is what makes payments reliable, reversible when needed, and compliant.

Equally important is the context: the information that moves alongside the funds. Payment messages transmit essential information for compliance and business operations, including Travel Rule data, invoice numbers, merchant details, and customer identifiers. This context allows businesses to reconcile payments with contracts, match them with invoices, and meet AML/CTF requirements.

Crypto transactions, by contrast, are unilateral and lack context. Whoever holds the private keys decides has full control to decide whether settlement happens. Without a pre-transaction authorization step or counterparty context, institutions have no way to vet, approve, or refuse incoming funds. Additionally, blockchains record only the amount, asset, and wallet addresses—no information about the counterparty, purpose, or which invoice it references.

Without a pre-transaction authorization step or counterparty context, crypto rails can’t power real-world payments. Businesses need to know who they’re transacting with, why a payment is being made, and whether it meets compliance criteria before funds move.

This is a key limitation stablecoins face today. They enable instant, global value transfer, but lack the context, trust signals, and institutional coordination that make payments truly work for businesses.

How the FATF Travel Rule Became a Catalyst for Crypto Authorization

When the FATF introduced the Travel Rule in 2019, it created the perfect conditions to build a compliant authorization layer for crypto. The rule requires counterparties in a virtual asset transaction to exchange originator and beneficiary information before settlement.

For the first time, crypto institutions were required to collaboratebefore a transaction occurred, mirroring the same pre-transaction authorization and due diligence flows that underpin traditional finance.

At Notabene, we saw this as a pivotal opportunity. The Travel Rule isn’t just a regulatory requirement—it’s an architectural upgrade. It gives the industry a shared standard to exchange trusted information, unlock counterparty confidence, and enable compliant, authorized crypto transactions at scale.

We’ve Already Built It: Pre-Transaction Authorization as Best Practice

Over the past five years, Notabene has turned Travel Rule compliance into an operational standard for the industry.

Today, more than 2,000 institutions across 100+ jurisdictions rely on Notabene’s open Transaction Authorization Protocol (TAP) to exchange verified transaction data and pre-transaction authorizations. To date, the Notabene Network has powered more than $1.5 trillion in compliant transaction volume.

Within our network, pre-transaction authorization has become an established best practice. Counterparties exchange compliance data, verify each other’s risk profiles, and explicitly approve transactions before funds move.

The Dilemma: Global Travel Rule Adoption Still Faces Gaps

Since the FATF introduced the Travel Rule in 2019, global implementation has expanded rapidly but unevenly.

According to the FATF’s June 2025 targeted review, 85 jurisdictions now enforce or have enacted Travel Rule legislation, up from 65 in 2024. 99 out of 117 jurisdictions had either passed or were in the process of passing relevant legislation at the time of the report.

However, only 35 jurisdictions have initiated active enforcement or supervisory actions. Nearly 60% of jurisdictions with legislation have yet to begin active Travel Rule enforcement.

Even where rules exist, VASPs face structural barriers to compliance. Because public blockchains are open settlement layers, VASPs cannot fully control the origin of incoming transfers. Many VASPs still lack the ability to reject deposits that arrive without verified Travel Rule data or from untrusted counterparties, which undermines their ability to maintain consistent counterparty risk controls.

This fragmented and inconsistent implementation, coupled with persistent technical interoperability challenges, limits the Travel Rule’s full potential. To unlock the next generation of payments, authorization and compliance must become built-in properties of the transaction, not optional layers added after the fact.

Notabene Flow: Stablecoin Payments with Authorization Built In

Enter Notabene Flow, the open stablecoin payments platform that makes authorization and Travel Rule compliance native to every payment.

Flow uses an addressless payments architecture: settlement addresses are revealed only after all Travel Rule information is exchanged and the required due diligence, consent, and compliance checks are completed. No address, no payment—and as a result, no possibility of unauthorized or non-compliant settlements.

Here’s how it works in a Pull Payment scenario:

- Payment initiation – The merchant’s payment service provider (PSP) issues an invoice and payment request in Flow, automatically generating a Travel Rule message that includes payee data and transaction details.

- Payment response – The payer selects their payment provider, who adds payer information to the Travel Rule record.

- Dual authorization – Both counterparties conduct compliance and risk checks.

- Settlement and disclosure – Once both counterparties have completed their compliance checks and authorized the transaction, the agent representing the payee sends an authorization message back to the agent representing the payer. This message includes the settlement address, which is revealed only at this stage. .

This model elevates pre-transaction authorization from a best practice to a built-in feature of every Flow payment. It also transforms the Travel Rule from an isolated compliance task into a requirement enforced by the design of the payment itself.

By revealing settlement addresses only after both sides complete authorization and exchange verified information, Flow makes it technically impossible to receive unvetted or non-compliant deposits. Institutions regain full control over inbound payment flows, strengthening their ability to apply consistent counterparty risk policies, prevent unwanted exposure, and enforce compliance at the protocol level.

Business-Ready Stablecoin Payments—Built for the Real World

Notabene Flow transforms stablecoins from fast settlement tools into a fully authorized, compliant, and business-ready payment network.

By combining the instant settlement of stablecoins with a pre-transaction authorization and compliance layer, Flow delivers what neither can achieve alone:

- Instant, borderless settlement without intermediaries

- Pre-transaction authorization, counterparty verification, and Travel Rule compliance

- End-to-end control and transparency across every transaction

With Flow, companies can finally unlock the efficiency of stablecoins — without sacrificing oversight, trust, or regulatory alignment.

This is the foundation for the future of B2B payments: instant, compliant, and ready for the real world.

Explore Notabene Flow and apply to become a Notabene Flow founding partner, accepting applicants until January 2026.

In this episode of Stack Chats, a new video series from Notabene, Pelle sits down with Anoosh Arevshatian, CPO of Zodia Custody, to talk about the complex world of custodial services in the digital assets space.

On September 29, Notabene Summit 2025 brought stablecoin operators, payment innovators, and compliance experts together in New York City to explore a critical question: how do we build the trust infrastructure that turns global stablecoin payments into a reality?

Against the Manhattan skyline, industry leaders gathered to discuss the $120 trillion B2B payments opportunity, and the role that stablecoins will play in capturing it. The timing couldn't be better. With regulatory clarity emerging in the US and institutional adoption accelerating globally, the conversation around stablecoin adoption has shifted from "if" and “when”, to "how."

These were the three defining insights from the day:

1. Trust Infrastructure Unlocks Institutional Adoption

Regulatory clarity was the first domino to fall. With the GENIUS Act now law and broader market structure legislation advancing, the US is finally signaling openness to innovation. As Chris Shimizu, AML Program Manager for Robinhood, put it after 14 years in crypto compliance: “It’s amazing to finally see this level of openness in the US.”

Now comes the harder part: turning that clarity into operational reality.

In the first two panels of the day, leaders from Blockchain Association, the US Treasury Department, Anchorage Digital, Talos, Apollo, Digital Asset, and DRW outlined what needs to happen next. Christine Moy from Apollo described the institutional trust challenge:

"You couldn't trust the technology because it was new and parametrically different from anything that you ever built internally at a centralized financial institution." —Christine Moy, Partner, Strategy (Digital Assets, Data, AI), Apollo

Mark DuBose from Anchorage summed up the moment:

"GENIUS was good for the United States. Clarity will be really good for the industry."

Regulatory progress opened the door. Now institutions need the tools to walk through it.

The operational barriers are formidable:

- Travel Rule compliance is required across jurisdictions with differing implementations

- Real-time counterparty verification is needed for multiple transaction participants

- Due diligence at scale is a significant operational burden

The principle repeated throughout the day was clear: trust can’t be outsourced to a closed network. Institutions need open, interoperable tools that let them enforce their own policies while operating at scale.

Regulation provides the framework. Trust infrastructure makes it work.

2. B2B Stablecoins Face a $120T Opportunity

The numbers are staggering: $120 trillion in annual B2B payment flows, and stablecoins currently capture 0.03% of it. The gap isn’t demand. It’s infrastructure that doesn’t yet serve real business needs.

During the Summit, Alice Nawfal walked through a simple example: a Portuguese clothing manufacturer paying a Turkish fabric supplier. This simple transaction involves five intermediaries, six SWIFT messages, transfer fees, and operational overhead at every step.

"Traditional banking rails were designed to optimize for domestic payments, not the kind of fast global trade businesses need today," Notabene's Pelle Braendgaard added.

Stablecoins natively solve one half of the settlement problem with 24/7 availability, low costs, and instant finality for sending payments. But their "push-only" transaction model leaves out essential B2B workflows: no pull payments, recurring billing, payment requests, nor dispute resolution.

The closing panel—featuring leaders from Walapay, Bitso, Mastercard, and Borderless—dialed up the urgency. Kevin Lehtiniitty of Borderless noted that one of the most common questions from TradFi companies is how to enable requests for payments — a capability that, until now, hasn’t existed. "How can we stop moving money on Telegram, please, as an industry," he pled with the audience.

Announced live at the Summit, Notabene Flow is the our next major product evolution: an open coordination layer for trusted B2B stablecoin payments. Built on Notabene's existing network of 2,000+ regulated entities processing $1.5 trillion annually, Flow combines three elements:

- Context - Provided by secure data messaging between entities, related to the transaction, and facilitated by the open-source TAP protocol

- Trust - Provided by 2,000+ trusted entities completing Travel Rule-compliant transactions on the Notabene Network today

- Authorization - Via Notabene Transact’s automated transaction authorization platform that allows counterparties to use custom policy engines to approve, reject, or flag transactions based on their own unique business needs and risk factors.

The combination of these three key elements is what allows us to build a payments layer on top of our existing network that can enable pull payments. This payment type, which includes recurring billing, payment requests, and subscription flows, is an essential capability that traditional businesses rely on —and a key reason that stablecoins have not yet been able to make a dent in the massive B2B payments market.

The result is near-100% straight-through processing rates and a pathway to scale compliant stablecoin payments across borders with no need for costly and burdensome bilateral banking relationships in each jurisdiction.

Anoosh Arevshatian from Zodia Custody (one of twelve Founding Partners of Notabene Flow, also including Bitso, Borderless.xyz, Dfns, Flutterwave, Gnosis, Monerium, Orbital, Portal, Walapay, Yellow Card) said of the launch:

"Compliance and trust aren't optional—they're the foundation of how we operate. That's why we value working with partners like Notabene, who embed instant counterparty trust into every transaction."

Mukul Tripathi from Mastercard added, "Notabene is very uniquely positioned to solve some of the very pressing pain points that exist in the industry with compliance first... making the whole ecosystem trustworthy."

Notabene CEO Pelle's Brændgaard summarized the vision:

"This is really why I got into crypto in the first place 15 years ago. We're going from being SWIFT for crypto to let's just be a better SWIFT."

3. Open Architecture Drives Adoption

The way payment networks are structured isn’t just a technical choice. Architecture determines which institutions can participate and how efficiently they can operate.

Kevin Lehtiniitty of Borderless.xyz highlighted the industry shift:

"A year and a half ago, VCs were saying 'you have issuers, blockchains, and on-ramps—we're done.' Now with Circle CPN and Fireblocks Network launching, people are circling back: 'Wait, maybe there's more to this.'"

Payment networks need to evolve in an open context rather than creating a series of walled gardens. Without that openness, the industry risks returning to the same limited structures that blockchain was supposed to improve.

The open vs. closed question is practical, not philosophical. Closed networks force binary choices: join our ecosystem on our terms, or build everything yourself. The practical benefits of open networks are clear:

- Implement your own counterparty verification policies

- Connect to multiple liquidity sources simultaneously

- Work with preferred compliance and custody providers

- Operate across jurisdictions with different requirements

Across the Summit, examples illustrated how open networks unlock real-world B2B payments. Ben Reid from Bitso is creating on-ramps for Mexican peso and Brazilian real stablecoins. Tom Borgers of Walapay is connecting emerging market corridors. Kevin Lehtiniitty of Borderless.xyz is building scalable transaction processing infrastructure. And Notabene Flow provides the coordination layer that ties it all together.

The pieces only work together if they're interoperable.

As Brændgaard put it:

"Crypto should be open, stablecoins should be open, payments should be open."

What’s Next?

The decisions made today will determine whether stablecoins scale in B2B payments or remain a promising but limited technology. To realize the opportunity, three building blocks must come together:

1. Trust infrastructure that institutions can build on: Not just compliance checkboxes, but tools for real-time counterparty verification and risk management at scale.

2. Payment coordination that serves real business needs: Pull payments, recurring billing, dispute resolution—the real-world capabilities that make large payment volumes work.

3. Open networks that preserve control: Interoperable infrastructure that lets participants maintain their own policies while gaining the benefits of coordination.

The validation throughout the 2025 Notabene Summit suggested that the industry recognizes what's needed. The companies building these solutions aren't waiting for permission. They're solving immediate problems for customers who need better payment rails today.

Stablecoins will transform B2B payments. The only question is how quickly we build the infrastructure needed to make it happen.

Let’s build it together.

Notabene Flow testnet is live, APIs and documentation ready, and Founding Partners already integrated. To learn more and join the open network, visit notabene.id/flow.

Notabene Flow introduces new business payment capabilities like pull payments and recurring subscriptions, enabling its fast growing network to tackle the huge addressable B2B payment market. The launch is backed by founding partners Bitso, Borderless.xyz, Dfns, Flutterwave, Gnosis, Monerium, Orbital, Portal, Walapay, Yellow Card, and Zodia Custody.

NEW YORK — September 29, 2025

Notabene, the trust layer for global money movement, today announced the launch of Notabene Flow—the first open stablecoin payments platform built for high-value cross-border business payments, on its active network of 2,000+ regulated entities processing over $1T annually.

The $120T global B2B payments market is massive, and while stablecoins provide faster and more efficient transactions, they account for only a tiny 0.03% of this volume. Their role remains limited because today’s crypto rails lack the trust infrastructure that traditional payment systems provide—capabilities like coordination, authorization, invoicing, and dispute resolution. Without these, companies struggle to prevent fraud, block illicit activity, and manage payment reversals. The result: stablecoin businesses are locked out of the larger B2B market or limited to one-way, push-only payments.

Notabene Flow unlocks this market by delivering the payment coordination and authorization layer missing from crypto rails. It introduces pull payments, recurring subscriptions, and compliant multi-party flows, all built on the strength of the Notabene Network—the world’s largest regulated crypto network, active in 100+ jurisdictions and processing over $5B in transaction volume a day.

“At Bitso, we have seen firsthand how stablecoins are a foundational layer for the next evolution of financial infrastructure, particularly in Latin America. But in addition to the value layer provided by stablecoins and the movement layer enabled by blockchain, an interoperability and compliance layer is required to fully bring this evolution to the most demanding institutional payment flows. Notabene addresses this directly with Notabene Flow, and building on a trusted existing network that provides the necessary layers of security and transparency is crucial for Bitso's growth strategy in cross-border business payments.”

—Ben Reid, Head of Stablecoins at Bitso

Having already tackled one of the industry’s toughest challenges—cross-border Travel Rule compliance—Notabene is now transforming their compliance core into a revenue engine. Notabene Flow’s open-loop network and transparent economic model incentivizes verified participants through revenue-sharing on competitively priced, stablecoin-powered transactions and reduced operational overhead and compliance costs, creating a virtuous cycle of adoption that rewards network participants while fueling sustainable growth of B2B stablecoin payments worldwide.

“Cross-border B2B payments have always been slow, expensive, and complex. Stablecoins are the first real opportunity to change that—but these high-value payments need a trust framework to succeed at scale. Notabene Flow delivers that framework, giving businesses the ability to run trusted, compliant payment flows with the efficiency of stablecoins and the reliability they expect from traditional finance.”

—Pelle Braendgaard, CEO, Notabene

Notabene Flow delivers immediate value through a single API integration that unlocks Travel Rule–compliant, multi-party B2B payment flows—making launching cross-border digital payments as simple as flipping a switch. With one integration, businesses gain instant access to an established and trusted global network that combines regulatory certainty with the flexibility of stablecoin and digital-asset payments.

“At Zodia Custody, compliance and trust aren’t optional—they’re the foundation of how we operate. Our institutional clients demand the same. That’s why we value working with partners like Notabene, who embed instant counterparty trust into every transaction. With Notabene Flow, a single integration point provides us the opportunity to expand stablecoin payments in a way that meets the highest standards of security and interoperability, with no heavy technical lift on our end."

—Anoosh Arevshatian, Chief Product Officer, Zodia Custody

Through a partnership with the Global Legal Entity Identifier Foundation (GLEIF), entity verification is anchored to the internationally recognized LEI standard, giving every participant a reliable foundation of counterparty trust. As of mid-September 2025, the Global LEI Index records just over 3.05 million LEIs issued worldwide, with more than 93% (~2.85 million) active. This reach and interoperability allows institutions to implement custom policy-based workflows aligned to their risk tolerance and jurisdictional needs—strengthening compliance while enabling faster, more scalable growth.

Notabene Flow is open-loop by design and built on the Transaction Authorization Protocol (TAP)—an open messaging standard that enables any verified entity to transact securely with trusted participants. Open-loop means no gatekeeping: no restrictions on assets, blockchains, jurisdictions, or membership tiers. Standardized messaging across the ecosystem enables trusted payment coordination with built-in Travel Rule compliance, eliminating the regulatory and operational burden of setting up separate entities, licenses, or bilateral agreements. Just as SWIFT standardized financial messaging for banks, TAP provides a common language for transaction authorization in the digital asset economy.

"As the first and one of the largest stablecoin payment networks, we believe mass adoption requires open standards - not additional walled gardens that create more fragmentation and slow growth. Companies already face a patchwork of providers, regulations, and jurisdictions, and the limits of push-only payments are clear. Having rolled out our network with leading stablecoin providers across 70+ countries, including Bridge, Bitso, and Yellow Card, we have seen firsthand the need for pull and recurring payments. We’re excited to partner with Notabene Flow to make this possible across our global on- and off-ramp network."

—Kevin Lehtiniitty, CEO, Borderless.xyz

Notabene Flow builds on the proven scale of the Notabene Network, trusted for over 5 years by more than 240 institutions to power fully compliant, multi-party transactions with straight-through processing rates above 85%. With the launch of Notabene Flow, Notabene cements its position as the de facto trust layer for global money movement—expanding beyond compliance to solve the broader challenge of enabling trusted, interoperable transactions across stablecoin rails.

Businesses can join the network today at notabene.id/flow.

About Notabene

Notabene is the trust layer for global crypto money movement, powering the largest Travel Rule-compliant transaction authorization network for regulated institutions globally. Our platform enables regulated entities across 100+ global jurisdictions to securely and seamlessly verify counterparties, authorize transactions, and comply with regulations—ensuring trust in every transaction.

With SOC-2 certification, ISO27001 compliance, and a strong focus on privacy and user experience, Notabene provides industry-leading tools for stablecoin payments, real-time transaction authorization, counterparty sanctions screening, and self-hosted wallet identification.

Headquartered in New York, Notabene operates globally with a presence in Switzerland, Singapore, Germany, and the United Kingdom. Trusted by over 240 companies, including Copper, Luno, Crypto.com, and Bitstamp, Notabene helps institutions build trust into every transaction while ensuring compliance with evolving regulatory frameworks.

Learn more at Notabene.id

Connect with us on LinkedIn | X

In this first episode of Stack Chats, a new video series from Notabene, Pelle sits down with Clarisse Hagége, CEO & Co-Founder of Dfns, to talk about stablecoin payments infrastructure and unique institutional needs.

US banking regulators have sent their clearest signal yet: the Travel Rule now applies to all banks offering crypto custody services.

In a July 2025 joint statement on crypto-asset safekeeping, the OCC, Federal Reserve, and FDIC outlined expectations for cybersecurity, operational resilience, and risk management. But one line in particular caught the attention of compliance teams: for the first time, US regulators explicitly named the Travel Rule as a compliance requirement for banks providing crypto custody.

Shifting US Regulatory Expectations for Crypto Custody and Travel Rule Compliance

The Travel Rule, first implemented under the Bank Secrecy Act (BSA) in 1996, requires financial institutions to transmit verified originator and beneficiary information with qualifying transfers. In traditional finance, it’s a cornerstone of AML compliance.

In the digital asset space, however, its application has long been debated. In the US, crypto (as “convertible virtual currency”) became explicitly subject to the Travel Rule when FinCEN issued guidance in 2013 and again in 2019, but the rule itself dates back to 1996. Many in the crypto industry have treated it as a requirement specific to crypto companies—something that only virtual asset service providers (VASPs) need to worry about, not banks.

The July 14 statement changes that. For the first time, US regulators have written the Travel Rule directly into formal interagency guidance for banks engaged in crypto custody:

“Crypto-asset safekeeping relationships are subject to applicable Bank Secrecy Act/anti-money laundering (BSA/AML), countering the financing of terrorism (CFT), and Office of Foreign Assets Control (OFAC) requirements … and follow the Travel Rule.”

— OCC, Federal Reserve, and FDIC, Interagency Statement on Crypto-Asset Safekeeping, July 14, 2025

This explicit mention transforms what was once implicit under broader BSA and AML obligations into a direct supervisory expectation.

How This Fits Into the Broader Regulatory Progression

This joint statement builds on a broader sequence of federal actions that have opened the door for national banks to offer digital-asset custody services. Find the complete timeline in our article on US banking regulators formally clearing national banks to engage in crypto custody.

What matters for this update is the regulatory trajectory: for the first time, the Travel Rule is explicitly written into interagency guidance for crypto-asset safekeeping, marking a shift from implied obligations to clear supervisory expectations.

Implications of Travel Rule Guidance for Banks

For banks entering or expanding crypto custody services, the joint statement removes longstanding ambiguity about compliance expectations. It makes clear that digital asset safekeeping is subject to the same regulatory rigor as traditional banking activities.

Key takeaways for compliance teams and leadership include:

- Compliance is explicit. The Travel Rule is now a named regulatory obligation, not an interpretive assumption.

- Identity-linked data sharing is required. Banks must be able to transmit verified originator and beneficiary information between counterparties.

- Architecture matters. Custody and ledger systems must support Travel Rule compliance, enabling secure data exchange and counterparty verification.

- Governance is essential. Boards, BSA officers, and compliance teams must integrate these requirements into their crypto risk management frameworks.

In short, Travel Rule compliance has evolved from a crypto industry best practice into a baseline expectation for banking supervision.

A Broader Signal for the Industry

The interagency statement doesn’t introduce new supervisory powers. It does, however, codify regulators’ view that Travel Rule compliance is integral to “safe and sound” digital-asset operations.

By positioning the Travel Rule alongside AML, CFT, and OFAC controls, regulators are signaling a convergence: the path forward for crypto custody depends on interoperable compliance infrastructure. Financial institutions will need solutions that make identity sharing seamless across ledgers, institutions, and jurisdictions.

Travel Rule Compliance as a Banking Baseline

The Travel Rule is moving from a crypto-industry guideline to a core requirement in US banking compliance. Firms entering or expanding crypto custody services must treat it not as an optional standard, but as a baseline obligation.

Compliance with the Travel Rule and transaction authorization need to be embedded from day one to operate safely, securely, and in line with regulatory expectations. Meeting these standards will be critical for both operational integrity and regulatory readiness.

Notabene Transact: The Trusted Approach to Travel Rule Compliance

Regulatory clarity is only half the challenge. Banks also need infrastructure that makes compliance operational. Notabene Transact provides that foundation.

Purpose-built for regulated financial institutions, Transact embeds pre-transaction authorization, counterparty verification, and Travel Rule compliance directly into the transaction flow. It automates decisioning before funds move, ensuring every crypto custody transaction is compliant, authorized, and secure.

With the world’s largest active network of Travel Rule–compliant entities, Notabene enables institutions to scale confidently as digital asset regulations mature. Notabene Transact turns Travel Rule compliance into a competitive advantage and a driver of trust. As regulators align expectations across traditional finance and digital assets, embedding trust and transparency into transaction infrastructure will determine which institutions lead the next phase of crypto adoption.

When the Financial Action Task Force (FATF) released revisions to Recommendation 16 (R.16) earlier this year, the headlines focused on “modernizing cross-border payment rules” and “championing transparency.” These goals sound good on paper, but the reality for financial institutions and virtual asset service providers (VASPs) is more complicated.

Compliance with R.16 is no longer just about transmitting fields like originator and beneficiary names. It’s about ensuring that every participant in a transaction is known, verified, and accountable. This requires standardized, high-quality information to flow seamlessly through complex global payment chains, while also embedding fraud prevention in every transaction.

The new standards demand greater coordination across financial intermediaries and technological innovation to handle evolving payment methods, including virtual assets, in a way that maintains both security and user privacy. This raises operational challenges but also opens the door for new solutions designed for the realities of crypto compliance.

Rules without real-world tools

The latest R.16 revisions aim to close gaps in payment transparency, requiring financial institutions to collect and transmit originator and beneficiary information throughout the payment chain. In practice, crypto payments and transfers are much harder than traditional currency to track.

Virtual IBANs and distributed wallets don’t map neatly to legal entities. Beneficiary verification, which is now a R.16 requirement, can be delayed or incomplete in instant-settlement crypto networks. Rigid data mandates, such as requiring geographic addresses, often do little to improve identification, and can even harm privacy or financial inclusion.

Without practical infrastructure, compliance becomes a checkbox exercise rather than a safeguard against fraud, money laundering, or sanctions violations. And without the right controls, real-world financial transactions can get messy, slow, or risky. That’s where the Transaction Authorization Protocol (TAP) comes in.

How TAP address real-world R.16 security challenges

TAP is an open-source, decentralized messaging protocol designed to securely and privately authorize and authenticate complex, multi-party digital asset transactions in real time. This enables compliant, scalable, and transparent global transaction flows across regulated entities, VASPs, DeFi, and self-hosted wallets.

TAP separates authorization from settlement, and gives institutions and VASPs the tools to build flexible, auditable workflows that meet their business needs while staying fully compliant with FATF regulations. It’s a protocol designed to address the practical challenges that FATF R.16 aims to solve, specifically with cross-border payments and virtual assets.

Here’s how TAP addresses the requirements established by R.16:

Separation of authorization and settlement.

R.16 emphasizes full transmission of originator and beneficiary information throughout the payment chain. TAP allows each transaction to be authorized before settlement, ensuring that all parties have verified the required information (names, IDs, compliance data) before funds move. This is especially important for crypto transactions, which settle instantly and irreversibly.

Built-in security and trust.

TAP creates a robust security layer that operates before any blockchain transaction is executed. By enabling the exchange of necessary information and requiring mutual agreement before settlement, TAP effectively mitigates the risks associated with unilateral and irreversible blockchain transactions. This pre-settlement framework allows for the detection and rejection of fraudulent or high-risk transactions, providing a crucial safety net that is often absent in standard cryptocurrency transfers.

Composable transaction workflows.

TAP supports flexible, threaded workflows (Transfers, Payments, Escrow, Swaps, Connect) that allow multiple participants to interact in a structured way. Each step references the previous one, creating an auditable chain of transactions that aligns with R.16’s goal of transparency in the payment chain.

Enhanced verification and compliance.

TAP enables pre-settlement verification: beneficiary institutions can confirm the accuracy of payment details and reject or authorize transactions as needed. Supports FATF-required data fields natively, making compliance built-in rather than an afterthought.

Dynamic participant discovery.

TAP allows for real-time discovery of all participants, including intermediaries and service providers. This ensures that the entire payment chain is known and auditable, solving the R.16 challenge of hidden participants and incomplete information flow.

Privacy and selective disclosure.

Sensitive data is shared only with authorized parties, allowing R.16 compliance without exposing unnecessary personal information.

Adaptable to virtual assets.

TAP solves key VA-specific R.16 challenges like virtual IBANs and blockchain addresses by using transfer requests instead of relying solely on account identifiers. Ensures accurate identification of counterparties and supports Travel Rule implementation for VASPs.

Making crypto payment transparency operational

TAP provides the infrastructure that makes full R.16 compliance feasible, especially for fast, complex, crypto transactions. It operationalizes transparency, verification, and compliance without slowing down transactions or compromising privacy. TAP also ensures pre-settlement verification and regulatory transparency without locking users into one system or region.

Open, permissionless, and auditable—TAP empowers financial institutions, VASPs, and regulators to move money with trust.

Download the whitepaper to learn more about the protocol.