What the End of MiCA Grandfathering Means for Crypto Firms in Europe

On 11 June, Notabene hosted a panel of leading policy and compliance experts to take stock of MiCA's implementation journey and look ahead to what comes next. Here's what we heard.

The EU's crypto regulatory experiment has entered its final chapter. On 1 July 2026, MiCA's transitional period ends across all member states. From that date, crypto asset service providers operating in the EU must operate under full MiCA authorization — no exceptions.

At the same time, the European Commission has opened a targeted consultation asking a pointed question: is MiCA, as written today, still fit for purpose? The consultation covers stablecoins, DeFi, offshore CASPs, tokenization, and the relationship between MiCA and broader EU financial regulation — opening the door to MiCA 2.0, even before MiCA 1.0 has been fully implemented.

To make sense of this pivotal moment, Notabene's Director of Regulatory & Compliance, Catarina Veloso, hosted a panel of senior experts from Bitpanda, VASPnet, Chainalysis, and Fireblocks for an honest assessment of where we are and where we're going.

What MiCA Got Right

The panel kicked off on a positive note. Acknowledging that despite implementation friction, the framework itself has delivered something meaningful: a harmonized regulatory perimeter that replaced a fragmented patchwork of national regimes.

Neil Samtani, CEO of VASPnet, put it directly: before MiCA, firms operated across 27 different national registers, with wildly uneven supervisory maturity — "silver and gold plating" practices that prevented a level playing field . MiCA replaced that with a single standard, a clear route to market, and genuine access to the EU single market via passporting.

"Today we have a mature, harmonized regulatory perimeter that's been drawn out — and that's especially valuable when you compare it to what things looked like pre-MiCA. There is a clearer route to market, and especially access to the single market, which is so important." — Neil Samtani CEO, VASPnet

Michał Truszczyński from Bitpanda made the operational stakes concrete: before MiCA, Bitpanda held 17 separate licenses and registrations across EU member states. One MiCA license now replaces that entire stack.

Matthias Bauer-Langgartner from Chainalysis highlighted a less-discussed benefit: MiCA has forced traditional financial services firms to engage seriously with crypto for the first time. He sees banks, MiFID firms, and EMIs now exploring stablecoin arrangements, custody, and trading platforms — participation that simply didn't exist before the regulatory legitimacy MiCA provided. Beyond its impact on market participation within Europe, Bauer-Langgartner also emphasized MiCA's growing role as a reference point for crypto regulation globally.

"MiCA has provided a global standard that is the baseline of discussions for other jurisdictions — which is extremely important, particularly around crypto assets, which are inherently global. It's not only a common standard for Europe, it actually sets the baseline for the international community, particularly the US and other jurisdictions now." — Matthias Bauer-Langgartner Head of Policy Europe, Chainalysis

Dea Markova from Fireblocks pointed to evidence of this institutional adoption in the licensing data. In some EU markets, roughly half of all CASP and issuance licenses have gone to banks or bank-affiliated entities, underscoring how traditional financial institutions are embracing the opportunities created by MiCA. Markova also observed that MiCA has attracted significant non-European players who are choosing Europe precisely because of the regulatory certainty it provides. Large global crypto firms are increasingly selecting EU member states as their MiCA domicile — a vote of confidence in the framework despite the compliance burden.

The Numbers Behind the Transition

Drawing on VASPnet's tracking of crypto businesses' regulatory footprints across Europe, Neil painted a striking picture of consolidation. Pre-MiCA, there were approximately 3,500 active VASP registrations EU-wide. Today, 1,700 transitional registrations remain active across member states still inside the grandfathering window — and just over 220 full MiCA licenses have been issued. His projection: roughly 400 CASPs will hold MiCA licenses once the dust settles.

But Neil stressed that this should not be viewed simply as a shrinking market. While some businesses exited the market amid more challenging regulatory and commercial conditions, much of the reduction reflects regulatory consolidation enabled by passporting: firms that previously maintained multiple registrations across Europe can now serve the entire EU under a single MiCA license. The numbers have also been shaped by M&A activity, as larger firms acquire smaller operators.

With around 60% of CASP authorizations concentrated in just five jurisdictions — Germany, the Netherlands, France, Malta, and Cyprus — some observers have questioned whether MiCA is encouraging regulatory arbitrage or a race among member states to attract crypto firms. Matthias pushed back on any reading of this as a regulatory race to the bottom. The concentration in Germany, the Netherlands, France, Malta, and Cyprus — roughly 60% of CASP authorizations — is, in his view, a direct product of pre-MiCA history. Germany required banking licenses for crypto custody before MiCA existed; France ran a full DASP regime. Firms that were already operating inside a proper prudential framework had a materially easier path to MiCA authorization than firms accustomed to AML-only registration. The licensing map, in other words, largely reflects where regulatory infrastructure was already built. He also drew an important distinction between where firms are licensed and where crypto activity actually takes place.. Spain and Italy — countries with far fewer licensees — rank alongside the Netherlands in the top five for on-chain transactional inflows.

That gap is passporting working as intended, but it is also, as Matthias put it, precisely why supervisory convergence across member states matters. A firm can be domiciled in one jurisdiction and serve customers across the bloc. If the NCA in that jurisdiction is under-resourced or slower to act, the entire EU's consumer base carries the risk.

The Offshore CASP Problem

With full MiCA supervision beginning, one of the most urgent enforcement questions becomes: what happens to crypto firms that are not authorized and continue to serve EU customers?

Neil walked through research VASPnet conducted on the top 78 centralized exchanges:

- 8 held a MiCA license

- 20 were operating under at least one legacy member state registration

- 50 had no EU regulatory presence — but their terms of service didn't restrict European business

That last figure is the enforcement challenge. MiCA's reverse solicitation provisions are tight — Michał noted that even making a product available in EU app stores, in EU languages, or at EU-targeted conferences could constitute solicitation. But enforcement requires NCA capacity that varies significantly across member states.

Neil's read on Article 19B of the Transfer of Funds Regulation is particularly significant in this context: if an EU-licensed CASP is transferring value to an offshore firm, that relationship carries correspondent-level due diligence obligations. In other words, the Travel Rule isn't just a compliance checkbox — it's becoming a mechanism to map and contain the offshore CASP problem from within the authorized perimeter.

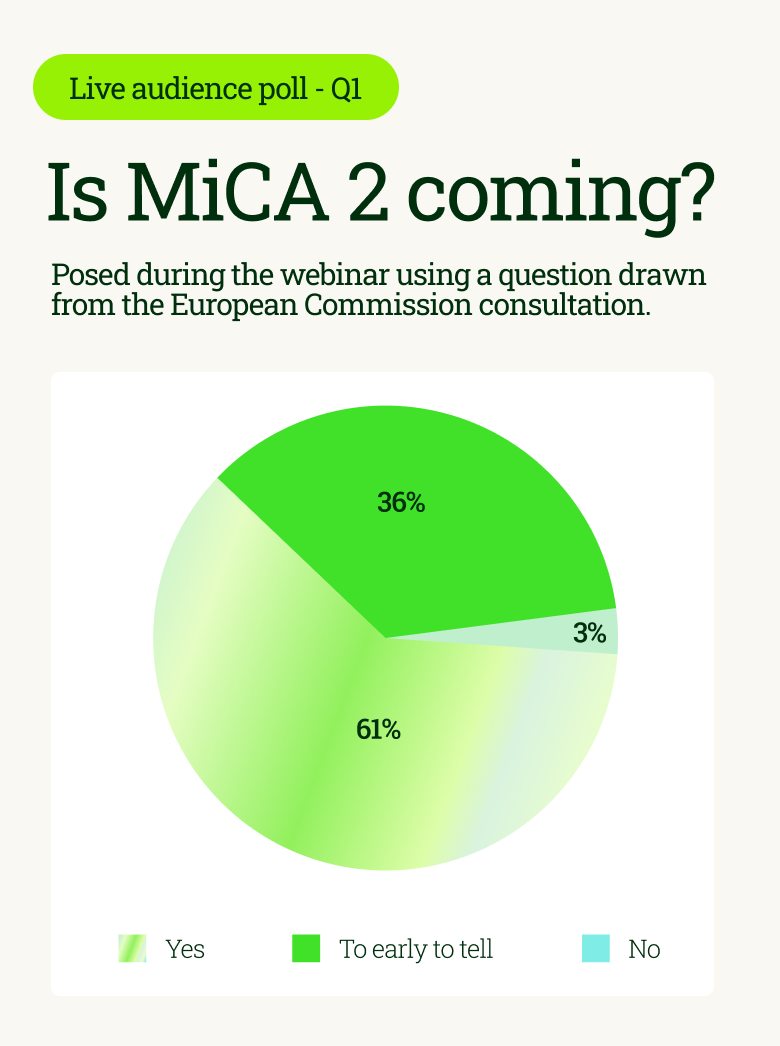

The MiCA Review: Fine-Tuning or Major Overhaul?

Here the panel's views were nuanced — and the audience's poll result was revealing.

When asked whether MiCA 2 is on the horizon, a clear majority of the audience expected a legislative follow-on.

Michał's reaction: Bitpanda would vote no on a major MiCA 2.0 overhaul.

"MiCA itself has 150 pages. The 47 implementing acts beneath it run to 2,000–3,000 pages. Add TFR and DORA, and you're looking at 5,000 to 10,000 pages of compliance reading in an industry that moves at pace. The ask from industry isn't a new framework — it's simplification and supervisory convergence."— Michał Truszczyński Senior Specialist Public Affairs, Bitpanda

The panel broadly agreed that the priority should be fine-tuning at levels 2 and 3. There are 47 implementing acts beneath MiCA's level 1 text — and beyond MiCA, firms must also contend with TFR and DORA running in parallel. The ask from industry isn't a new framework — it's simplification, coherence, and supervisory convergence across member states.

With firms and regulators still adapting to MiCA, launching a new legislative process too soon could create uncertainty, divert resources from implementation, and risk disrupting a framework that is only beginning to deliver the benefits of regulatory harmonization. The consensus was that Europe should focus first on making MiCA 1 work as intended before considering a more ambitious second phase of reform.

The Stablecoin Question

Euro-denominated stablecoins were a key discussion topic for the panel — and to ground the conversation in live audience sentiment, we put a question drawn directly from the Commission's consultation to the room:

The results didn't go unchallenged. Dea pushed back on the skeptical reading. While acknowledging that domestic payments within the Eurozone don't have much friction, with SEPA and instant payments regulation having done significant work, the case for euro stablecoins, she argued, is strongest elsewhere: cross-border and programmable payment contexts, intraday yield, AI-native payment flows, and tokenized money market fund access all become meaningfully easier with a euro-denominated on-chain asset.

By creating efficient, regulated payment rails between Europe and key international corridors, euro stablecoins could allow more value to move directly in euros rather than requiring conversion into dollars or local currencies at multiple points in a transaction. In that sense, stablecoins could strengthen the international role of the euro by embedding it more deeply into digital payment infrastructure.

Matthias agreed with the direction but noted the scale reality: less than 0.5% of on-chain crypto activity is currently denominated in euros. The deepest, most liquid pools remain dollar-denominated. The opportunity for euro stablecoins is real, but demand and liquidity still have a long way to go before they can rival the dollar's dominance.

The Multi-Issuance Debate

Closely related is the multi-issuance question: can the same stablecoin be issued through separate legal entities in different jurisdictions, and how does that interact with MiCA's reserve, redemption, and supervision requirements?

Matthias framed the multi-issuance debate as one of MiCA's most difficult unresolved questions: how to preserve the global utility and fungibility of stablecoins while maintaining European supervisory standards and consumer protections. He noted that stablecoins are inherently global instruments, with cross-border payments among their clearest use cases, yet MiCA must also account for concerns around monetary sovereignty, reserve location, and redemption rights for EU holders. Splitting a stablecoin into separate EU and non-EU versions may look attractive from a supervisory perspective, but in practice it risks fragmenting liquidity, duplicating smart contract infrastructure, and making the token less useful across both DeFi and centralized markets. For Matthias, the challenge is supervising global stablecoins without undermining the very cross-border functionality that makes them valuable. Enhanced supervisory cooperation, such as the recent EBA–NYDFS memorandum of understanding, may be an important step toward that balance, but the path to globally usable, well-supervised stablecoins remains complex.

What Comes Next

Two important milestones now sit directly ahead of the industry. On July 1, MiCA's grandfathering period comes to an end across the EU, closing the transition window that allowed firms to continue operating under pre-MiCA national registrations. At the same time, the European Commission's consultation on the future evolution of MiCA remains open until 31 August, inviting industry feedback on everything from stablecoins and global issuance models to DeFi, staking, and tokenized deposits.

As Michał explained, the expiry of the grandfathering period should bring the market closer to a true level playing field. Firms operating in the EU are expected to be authorized under MiCA, reducing the inconsistencies that existed under the previous patchwork of national regimes.

The next test is supervision. Michał emphasized that tighter enforcement will be essential, but also acknowledged that this remains new territory for national competent authorities. NCAs differ in resources, risk appetite, and supervisory focus, and the interaction between home and host member states — and with ESMA — will become increasingly important.

The consultation raises a different but connected question: how much MiCA should now evolve. Dea's view is MiCA should be improved, not reinvented. The first draft was written roughly six years ago, in response to a very different market environment. Since then, particularly in payments, use cases for stablecoins have become far more concrete. For Dea, that makes the consultation a timely opportunity to be somewhat bolder in revisiting the payments titles, while preserving MiCA's broader architecture.

The panel's message was consistent: the priority is to make MiCA work in practice, while using the consultation to identify targeted improvements where experience has exposed genuine gaps.

Watch the full webinar on demand → https://notabene.id/webinars/from-transition-to-transformation-mica-grandfathering-ends

Notabene is the trust layer for global crypto money movement.

Notabene Flow — the first open stablecoin payments platform for businesses—and Notabene Transact—the world's largest Travel Rule-compliant transaction authorization platform for regulated institutions—are built on the Transaction Authorization Protocol (TAP), an open messaging standard that enables verified entities to transact securely.

The Notabene Network connects thousands of trusted counterparties, facilitating over $1T in transaction volume annually across over 100 jurisdictions.

Subscribe to Notabene Blog

Subscribe to our product updates, news on crypto regulations and more

Request a demo

Notabene offers a demo for you to learn and understand how to use our products

Book demo